It all started with a dream or a vision, didn’t it?

However, as your business grew, so did the challenges, such as managing cash flow and running short on funds, which became a roadblock to achieving that vision. What if you had the support to move forward and take that next big step?

Here’s where the government subsidy loan for businesses and other MSME schemes can help. This type of subsidy loan scheme for businesses makes borrowing more accessible and cheaper.

In this blog, I’ll walk you through the entire process from finding the right scheme and subsidies to applying for them. Let’s get you the money you need to grow!

I’ll explain to you the government subsidy loan for business with a quick example –

Suppose you want to purchase a set of equipment and computers to support your business’s expansion. Usually, in this situation, you’ll go to the bank asking for a loan.

Here’s where a government subsidy loan comes in, where the government pays part of your interest to the bank, which means you end up paying a much lower interest rate.

In India, these schemes can come in the form of low-interest loans, direct cash support (similar to gov small business grants), tax benefits, and support for maintaining minimum prices.

Let’s understand a few more benefits of taking government subsidy loans –

Lower-interest loans make it easier for new entrepreneurs to start and help established businesses expand.

As your business grows, you’ll need a team to handle the workload. These types of loans can give you the confidence to create jobs and help the community as well.

The MSME sector is an important part of India’s economy, and when your business does well, it helps the whole country’s economy. These loans allow you to contribute more to the nation’s growth.

With these special schemes, the government often focuses on helping specific areas like farming, clean energy, and businesses run by women or underrepresented groups.

With reduced interest, you have more money to reinvest in your business for hiring, upgrading machinery, or expanding your reach.

I’ve seen this problem where many MSME business owners don’t even consider taking an msme subsidy loan from the bank because they think the interest rates are too high, there is a lot of paperwork, and the collateral requirements are too heavy.

However, let me assure you that a government subsidy loan for business is different and much easier to apply for, with low interest rates.

Let’s talk about how these special government business loans are different from regular bank loans and why they might just be the support you need to grow your business.

| Subsidy Loan | Regular Loan |

| A part of the interest is paid by the government, which means lower EMIs | Higher interest rates are set by banks based on market conditions, which means higher payments are required over time. |

| Subsidy Loan | Regular Loan |

| Often, no property is needed as the government backs these loans. | Property or assets are always required, which can become a barrier sometimes. |

| Subsidy Loan | Regular Loan |

| Based on specific government rules that consider business types, location, background, and exceptional support for women-backed businesses. | Primarily based on income and financial history |

| Subsidy Loan | Regular Loan |

| These loans are designed and support national goals like job creation and rural growth in specific regions | It can be used for any business purpose, offering flexibility without extra benefits. |

| Subsidy Loan | Regular Loan |

| Often have online application processes for faster approvals, sometimes within days | Involves extensive paperwork and a long waiting period for financial review and approvals. |

It’s a relief to know these options exist. The real question is what to fix first in your business. A one-on-one business coaching helps you find that clarity.

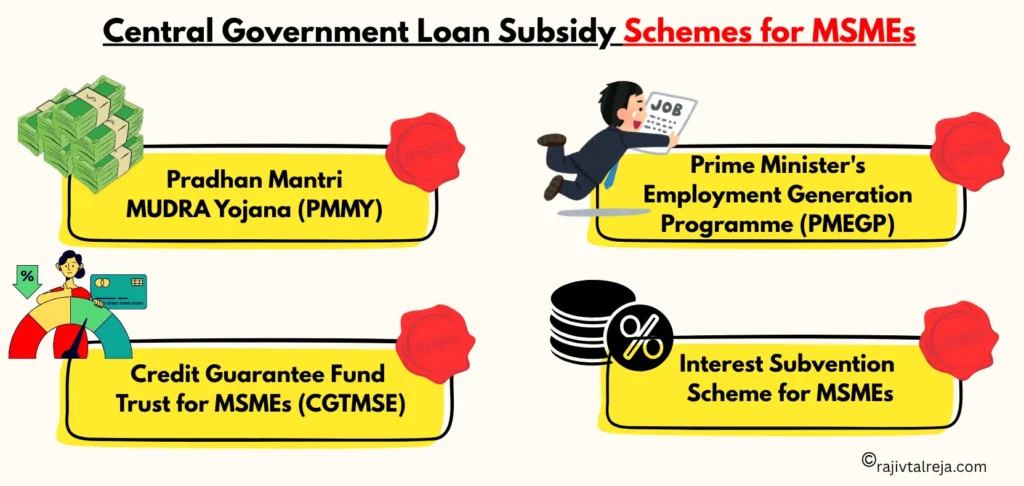

Now, I’m going to break down the details of each central government subsidy loan for business available for MSMEs.

Coach tip – Don’t ignore these schemes. Their sole purpose is to help business owners grow their businesses without being overwhelmed by heavy debt. These loans come with low interest rates, no need for security, and are easy to apply for.

Let’s break it down one by one –

This scheme was made for small business owners who need funds to start, run, or grow their business. It’s been around since 2015 and is super useful. The Mudra loan subsidy ensures that interest rates remain affordable for small businesses.

The PMMY smartly categorises loans based on the stage and needs of your business. This ensures you get the right amount of funding at the right time.

This loan scheme was launched in 2015 by the central government for MSMEs that need funding to start, run, or grow their businesses. This scheme categorises loans into your current stage and the needs of the business.

This scheme is primarily structured into three categories or stages –

You can apply for a PMMY loan online through the JanSamarth portal. Here’s what you’ll generally need:

This is especially important for business owners who are planning to start. PMEGP is one of the most important government subsidy loans for new businesses.

PMEGP was launched in 2008 to create jobs through supporting the building of successful businesses in both rural and urban areas.

In the PMEGP, the government pays a fixed percentage of the loan that you don’t have to pay back. This percentage is the subsidy rate, which is categorised into general and special categories.

This scheme is important for MSMEs that lack collateral for business loans.

CGTMSE is a collaboration between the Ministry of Micro, SME, and the Small Industries Development Bank of India (SIDBI), started in 2000. CGTMSE is a prime example of a small scale industry loan subsidy program, especially designed for MSMEs in India who don’t have property or assets to offer as collateral for a business loan.

Loans up to Rs. 5 crore are available in the CGTMSE.

However, the maximum credit risk taken by the government is Rs. 3.75 crore under CGTMSE.

Note – if you don’t have a Udyam Registration Certificate, you can easily apply here.

The ISS for MSMEs was introduced in 2018 to ease the burden of high interest rates on business loans, allowing business owners to get the funds to grow and modernise their businesses.

Interest Subvention Scheme gives a discount of 2% on the interest you pay on new loans. This means you’ll be paying 7% only if the standard interest rate is 9%.

We’ve just covered the main Central Government loan schemes.

Now, let me take you to the next step: state subsidies and specific schemes that can further support your business growth.

The Indian government has specific programs beyond MSME loans to help businesses, including dedicated options for a government subsidy loan for small businesses. They’re targeted to solve specific challenges. Let’s explore these business-specific government loan options.

These schemes, especially launched to help:

| Government Loans for Startups | |

| Startup India | Tax breaks, simpler rules, fast-track support and access to the Seed Fund. |

| Startup India Seed Fund | Up to ₹20 lakh (prototyping) and ₹50 lakh (market entry, commercialisation, or scaling up) for early-stage. ((less than 2 years old) |

| Credit Guarantee for Startups | Collateral-free credit guarantee on loans up to Rs. 2 crore. |

| Atal Innovation Mission | Support for innovation, workspaces, mentorship, and funding. |

| MSME Business Loans in 59 Minutes | Loans up to Rs. 5 crore approved online |

| Loans for Women Entrepreneurs | |

| Stand-Up India Scheme | Loans of Rs. 10 lakh – Rs. 1 crore for starting new ventures, mostly collateral-free. |

| MUDRA Yojana | Collateral-free loans up to Rs. 10 lakh (Shishu, Kishor, Tarun categories). |

| Mahila Udyam Nidhi Scheme | Financial help up to Rs. 10 lakh and with easy repayment terms |

| Annapurna Scheme | Loans up to Rs. 50,000 for women in the food business. |

| Mahila Coir Yojana | Financial aid for equipment and training for the rural coir industry |

| TREAD Scheme | Financial aid + skill development for economically weaker women |

| Loans for Minority Business Owners | |

| Term Loan Scheme | Up to Rs. 20 lakh (6% p.a.) for income up to Rs. 3 lakh. Up to Rs. 30 lakh (8% p.a.) for income up to Rs. 8 lakh and 2% discount for women |

| Micro-Finance Scheme | Up to Rs. 1 lakh (7% p.a.) & Rs. 1.5 lakh (10% p.a.) and a 2% interest concession for women |

| Virasat Scheme | Up to Rs. 10 lakh for artisans at concessional interest rates |

| Loans for SC/ST Business Owners | |

| Stand-Up India Scheme | Loans of Rs. 10 lakh – Rs. 1 crore for starting a new business, often collateral-free. |

| NSFDC Micro-Credit Finance | Rs. 1.25 lakh loans at 6.5% interest |

| Mahila Samriddhi Yojana | Rs. 1.25 lakh for SC women at 6% interest |

| Suvidha & Utkarsh Loans | Higher-value loans for bigger projects (up to Rs. 9 lakh at 8%, Rs. 45 lakh at 9%). |

| Green Business & Mahila Kisan Yojana | Eco-friendly/agriculture loans for SC women |

| National Scheduled Tribes Finance and Development Corporation (NSTFDC) | Soft loans and subsidies for sustainable livelihood activities under the AMSY and ASRY schemes. |

| State | Key MSME Scheme | Benefit |

|---|---|---|

| Gujarat | MSME Assistance Scheme | Capital investment subsidy + interest subsidy for new enterprises |

| Maharashtra | Package Scheme of Incentives (PSI) | Industrial promotion subsidy, stamp duty exemption, electricity duty waiver |

| Tamil Nadu | MSME Special Incentives | 25% capital subsidy for manufacturing units (up to Rs. 30 lakh) |

| Karnataka | New Industrial Policy | Investment subsidies, interest-free loans, stamp duty concession |

| Uttar Pradesh | MSME Promotion Policy | Capital interest subsidy, exemption on electricity duty |

Visit your state’s Industries Department or MSME portal.

Most states publish their incentive schemes online. You can also check with your local District Industries Centre (DIC). They’re specifically set up to guide business owners through state-level schemes.

Don’t leave this money on the table. Many business owners only look at central government schemes and miss out on state benefits that can stack on top.

Many business owners miss out on these government schemes because they become confused by the process. So many schemes, so many rules!

Let’s understand how to get a government loan in a simple way, including how to apply for it and the process involved.

Before you apply for government loans, check these basic requirements –

Once you’ve applied online, banks or officials will check your plan and documents. They’ll review everything. If approved, follow all usage rules and ensure timely repayment.

You now have the complete roadmap to secure government funding. Are you ready to learn the systems that will ensure you turn that funding into extraordinary results? Build a proven execution system with India’s leading business coach.

My goal here is to help you take the next step and drive results for your business.

You can use this article as a starting point for your government subsidies list. The government has introduced various schemes to support MSMEs, but they can only help if you know how to use them wisely.

Take advantage of a government subsidy loan for business, other subsidies, and no-collateral support designed to help your business grow.

From understanding loans to mastering growth. We’ve got you covered. Click here to unlock more financial strategies for your MSME.

The MUDRA Yojana Shishu loan (up to Rs. 50,000) is the easiest to get. It requires minimal paperwork, no collateral, and can be applied for online through the JanSamarth portal.

No. Most government subsidy schemes require Udyam registration at minimum. Some also require GST registration. Register your business on the Udyam portal before applying.

Not always. Schemes like MUDRA, PMEGP (under Rs. 10 lakh), and CGTMSE specifically offer collateral-free loans. The government guarantees a portion of the loan to reduce the bank’s risk.

It varies by scheme. MUDRA loans through the JanSamarth portal can be approved within days. CGTMSE claims are typically processed within 48 hours. PMEGP may take a few weeks depending on your district.

Yes, in many cases you can benefit from multiple schemes. For example, a CGTMSE-backed loan combined with the Interest Subvention Scheme. However, avoid applying for multiple loans simultaneously as it can hurt your credit score.

Yes. The Stand-Up India scheme, Mahila Udyam Nidhi, Annapurna Scheme, and special categories under MUDRA and PMEGP all offer preferential terms for women business owners, including higher subsidy rates and lower interest.

While there’s no universal minimum, most banks prefer a CIBIL score of 650 or above. A higher score improves your chances of faster approval and better terms.

No. PMEGP is only for new businesses (first-generation units). If you already have a running business, look at CGTMSE, MUDRA, or the Interest Subvention Scheme instead.

Government subsidy loans are still bank loans. Non-repayment affects your credit score and can lead to legal action. The subsidy reduces your interest burden, but the principal must be repaid on time.