You don’t search “importance of financial review” on a happy afternoon.

You search for it when something feels wrong.

Sales are growing. Orders are coming. The team is busy. But your bank balance looks weak. GST is due. Your supplier is calling. You are wondering, “If business is growing, why am I always short of cash?”

This confusion is common across MSMEs in India. The problem is that business owners lack a structured financial review.

This article will give you a practical way to evaluate your current business situation. Let’s start with the basics.

A financial review is a focused check of your business numbers to see if they are accurate, healthy, and moving in the right direction.

It is not a FULL AUDIT.

It is a practical REVIEW that compares performance, asks questions, and highlights risks before they become serious problems

The importance of financial review is much greater than most owners realise. It is your early warning system. It helps you –

Without a financial review, you are reacting to problems.

With it, you are preventing them.

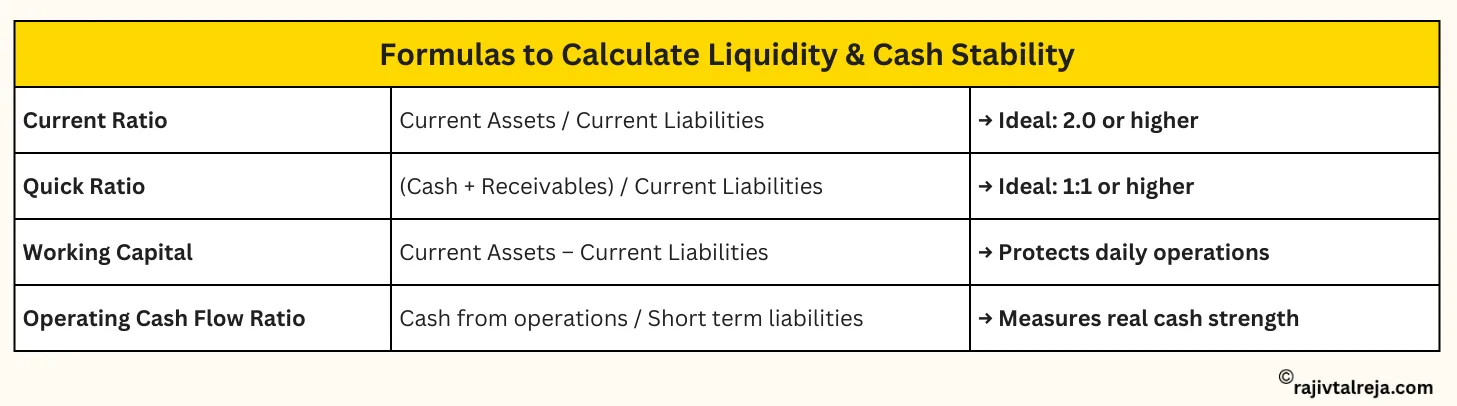

| The Numbers That Decide Your Business Stability – A Current Ratio below 1.0 signals possible liquidity stress. – DSCR below 1.25 raises loan rejection risk. – Positive Working Capital protects daily operations. |

Most owners don’t realise the real importance of a financial review until cash pressure begins.

If you search online, you will find advice like –

“Track EBITDA.”

“Improve shareholder value.”

“Optimise capital structure.”

But does that help you pay salaries?

Most content is written for large US companies with board meetings and investors. You’re handling cash, GST, credit, and staff daily.

You don’t need complex formulas. You need clarity:

Let’s focus on what actually matters.

| You don’t need complex corporate jargon. You need practical clarity. A dedicated MSME business coach can show you how to manage cash flow and prepare for real, profitable growth. |

If your business were admitted to a hospital today, what would doctors check first?

They would not ask about your turnover.

They would check your vital signs.

Your business also has vital signs. If even one goes weak, the whole system suffers.

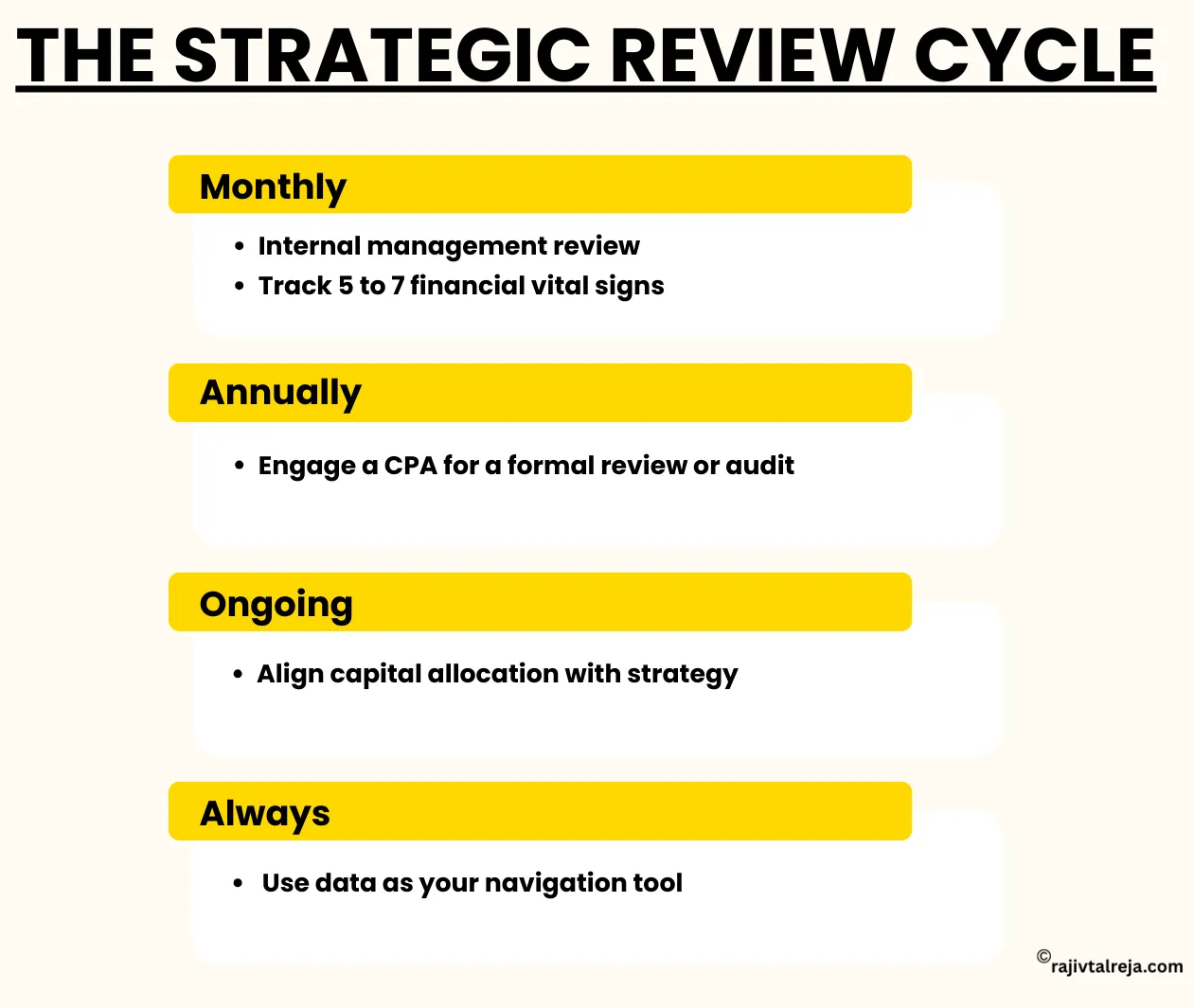

A monthly review ensures proper performance evaluation.

Let’s go through the 9 financial vital signs you must review every month.

Sales growth is good, but only if it stays above your break-even point.

Check –

If sales are growing but profit isn’t, leakage has started.

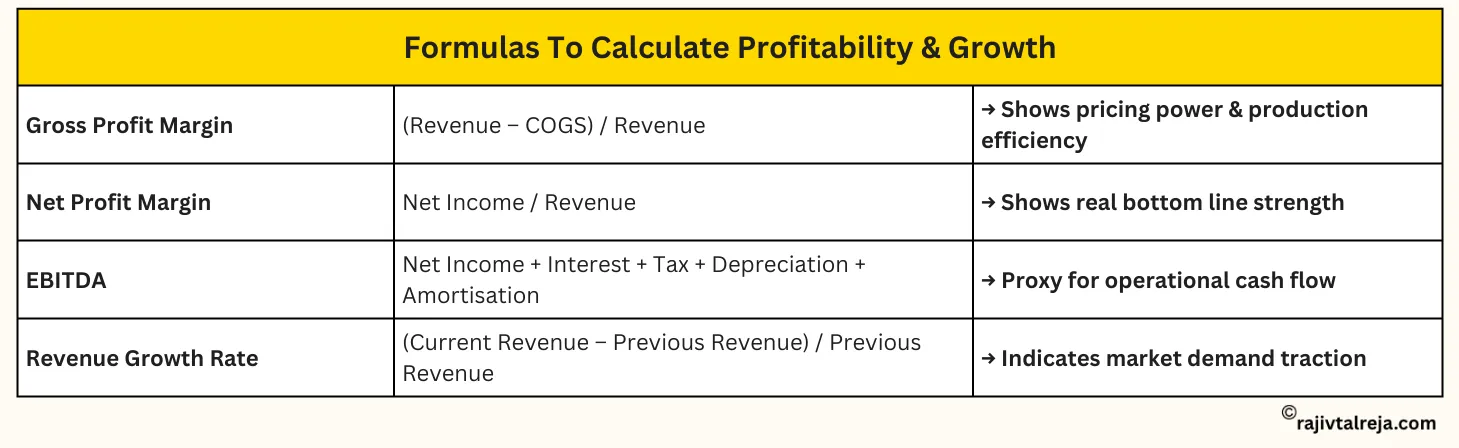

Many owners confuse gross profit, EBITDA, and net profit.

You must clearly see –

If interest and tax are eating too much, your business is working for the bank, not for you.

This is a real performance evaluation, not guesswork.

Imagine your revenue filling a bucket.

If there are holes, fixed expenses, variable wastage, commissions, money leaks out silently.

Check –

If expenses are rising faster than sales, danger is building.

A profitable business can still die if cash is stuck.

Strong cash flow management is the oxygen of your business.

Check –

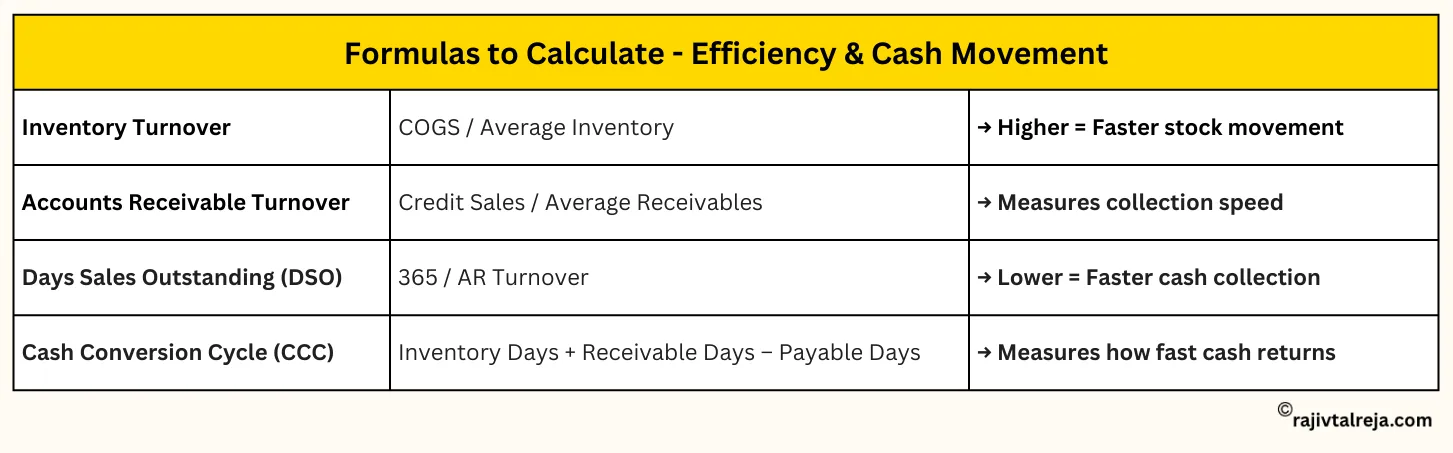

Who has not paid you?

How many days overdue?

What is your credit cycle length?

If receivables are stretching beyond 60 days, you are funding your customers’ business.

Track receivable turnover.

If collections slow down, your growth slows down.

Without disciplined cash flow management, growth creates stress.

| If you are looking at these vital signs and feeling overwhelmed by the numbers, one-on-one business coaching can help you diagnose exactly where your cash is stuck. |

Inventory is not an asset if it doesn’t move.

Identify –

If inventory moves slowly, your money is frozen on shelves.

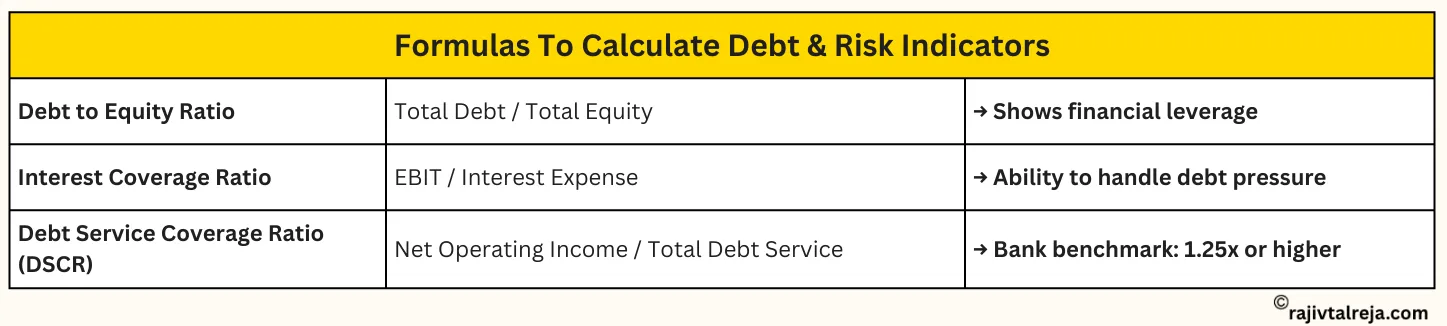

If EMI crosses 40% of profit, you are in the risk zone.

Check –

If DSCR is below 1.25, stress will increase.

Debt control is strong risk management.

Too much debt means you are working to pay interest, not to build wealth.

GST, TDS, Income Tax, and PF, if delayed, penalties compound.

A small compliance delay today can become a legal crisis tomorrow.

Review –

Timely filings are basic risk management.

Compliance is not optional. It protects your business reputation.

Are you investing in –

Or are you pulling all profits out?

Reinvestment must align with your financial goals.

If you don’t reinvest smartly, competitors will overtake you.

These 9 financial vital signs are early warning signals.

Use our Monthly Financial Vital Signs Template made for MSMEs to get started.

If you check them monthly, you will spot problems before they become emergencies.

The minimum review takes 30 minutes on the 5th of every month.

Open –

Ask – Can I survive the next 45 days comfortably?

If the answer is no, act immediately.

Focus on –

If you know these five clearly, you understand your business health.

Clear data improves decision-making under pressure.

Hiring non-revenue staff, accepting long-credit orders, buying machinery on EMI, and signing new leases.

Ignore complex words. Focus on money coming in, money going out, and money stuck. Ask your accountant to explain in simple language.

Common invisible mistakes –

The Owner, Accountant, Sales Head, and Purchase Head.

Sales bring revenue. Purchase spends money. Finance alone cannot control business.

A bad review is when the CA prints a 40-page report, you nod, ask only about the tax amount, and the meeting ends.

This does not help you reach your financial goals.

A good review ends with clear actions, like following up on debtors or cutting specific expenses.

Financial review is not about accounting perfection.

It is about clarity.

By checking these 10 areas, you stop guessing and start leading. You will sleep better knowing exactly where your money is and how to grow it.

Start with one simple habit –

On the 5th of every month, sit down for 30 minutes and review your numbers honestly.

You don’t need more sales first. You need financial clarity first.

Read more practical MSME growth blogs that help you build clarity, control cash, and scale with confidence.

To improve decision-making and strengthen cash flow management.

They simplify complex data so you can make better decision-making choices.

Balance Sheet, Profit and Loss, Cash Flow, Equity, Notes.

Review checks health monthly. Audit verifies records formally.