That weakening feeling in your stomach when you look at the pile of unpaid bills, the constant calls from suppliers, and the looming payroll date…

It’s a feeling every business owner fears. In these situations, the term “insolvency” might pop into your head, sounding like the final nail in the coffin for your business’s insolvency.

But what if it’s not?

What if it’s a red flag, a fork in the road that, with the right guidance, can steer your company not to its demise, but to a tougher, more adaptable future?

Let’s walk you through the storm and back to stable ground.

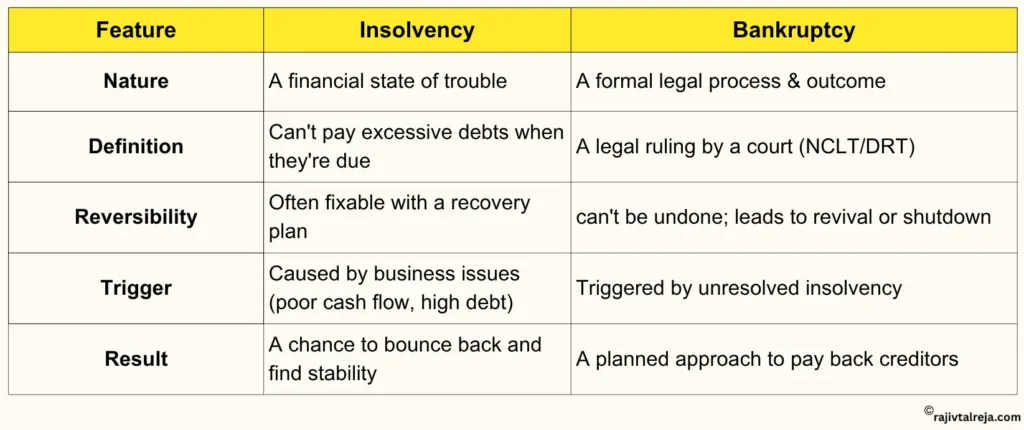

Business insolvency is about your money situation, not a legal penalty. It happens when your business’s insolvency can’t pay its bills on time.

If you are in these situations, you’re dealing with cash flow insolvency.

A lot of business owners mix up these words, but they’re quite different. Once you get it, you’ll feel more in control.

Insolvency means you can’t pay what you owe. It’s a tough spot, but often you can turn things around if you take the right steps.

Bankruptcy is the official legal way to deal with insolvency that won’t go away. In India, there is a law in place called the Insolvency and Bankruptcy Code 2016 (IBC).

Look at it this way – Insolvency is the sickness. Bankruptcy is the official announcement of death or the beginning of a court-monitored emergency treatment.

A company doesn’t go broke in one day.

For MSME businesses in India, a few causes of insolvency.

This isn’t about blaming anything, but finding the main problem so you can come up with an effective solution.

This is the most common internal reason small businesses face failures.

Cash flow is the lifeblood of your business, and when it stops flowing, everything else seizes up.

Check for these common traps –

Debt helps businesses grow, but the wrong kind of debt can lead to bankruptcy. Indian MSMEs face a big credit gap, which means many good companies can’t get bank loans.

This forces them to –

A business’s financial health is connected to its potential to sell its products or services effectively. If you don’t analyse and correct the slightest dip in revenue, then it is a direct threat to your solvency.

This can happen due to –

Small firms have limited money saved up, which makes them very open to sudden money problems. What might be a minor issue for a large company can be a fatal blow for an MSME.

These cash flow and debt traps are exactly what an experienced MSME business coach helps you anticipate and systematically dismantle.

The law, especially the Insolvency and Bankruptcy Code (IBC), is now designed with a “rescue culture” in mind, particularly for MSMEs. It gives you, the business owner, powerful tools to guide your company back to safety.

This 5-step framework gives you a practical guide to steady your business and lay the groundwork for a comeback.

A strong plan is also your best tool to convince creditors to team up with you.

You won’t be able to solve a problem you don’t understand.

You’ll need three key papers to know your financial health – your Income Statement, Balance Sheet, and most importantly, your Cash Flow Statement.

With these in hand, ask the tough questions to identify the causes of insolvency..

Work out these key ratios to get a quick assessment –

This shows if you can cover your immediate bills without having to sell your stock. A ratio under 1.0 raises a red flag.

This reveals if you rely too much on borrowed money.

The top goal is to stop money loss and save every rupee of cash. Take a hard look at all your costs.

Stop all non-vital expenses right away – work trips, dining out, subscriptions you don’t really use, and ads that don’t prove their worth.

Ask your main suppliers for better payment plans. Sell off any slow-moving stock that’s holding up cash. Use software like accounting tools to make these tasks easier.

Avoiding your lenders is the worst decision. It breaks trust with lenders. Open, honest communication is the only right way to go.

Before you pick up the phone, make sure you have the financial info from Step 1 at hand. Know what you can offer.

Don’t just ask for more time. Suggest a specific plan.

For example – “Can we stop payments for 60 days while we put our turnaround plan into action?”

Don’t just focus on the interest rate. Ask if you can pay over a longer time to lower your monthly costs, or if they can drop late payment fees.

A turnaround often requires a new cash investment, but regular banks refuse to lend to businesses in trouble. This is where alternative financing becomes a lifeline.

Sell your unpaid customer invoices to a finance company and get up to 95% of the cash immediately.

This is one of the fastest ways to solve a cash flow crunch caused by slow-paying customers.

Get a line of credit based on the value of your assets, such as inventory or equipment.

You get capital in exchange for a share of your future monthly income. The payments adjust, going up and down with your sales.

This is the final step that brings everything together into a single, professional document.

This plan is your roadmap for recovery from your business insolvency and your key to getting creditors and investors on your side. It must include –

A clear report on what went wrong (a SWOT analysis works well here).

Clear, measurable goals (For example, “Achieve positive cash flow in 6 months,” “Reduce debt by 15% in one year”).

The exact financial and operational changes you’ll make.

A realistic, fact-based 13-week cash flow forecast. This industry benchmark shows you have a solid plan to survive the near term.

Who’s in charge of what, and when it’s due, so your business regains financial stability.

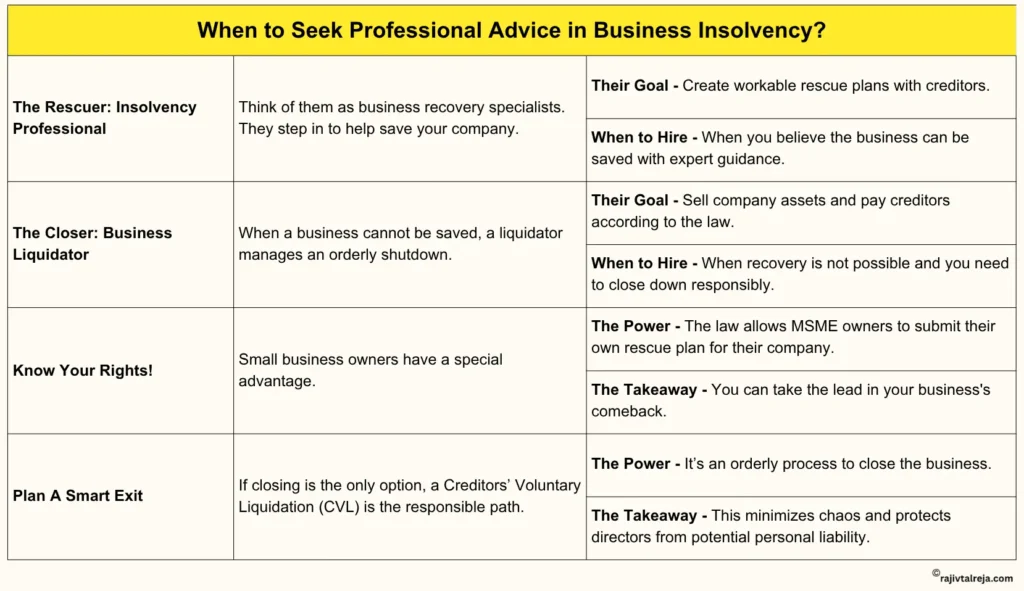

You can start the 5-step plan on your own, but dealing with major money troubles and legal matters often needs a pro to guide you.

Getting help from an expert is a smart move to boost your odds of making it through.

Professional guidance is the accelerator for your comeback. See why thousands of MSMEs trust Rajiv Talreja business coach, to help them build a resilient future.

A business insolvency is one of the toughest journeys an entrepreneur will ever take. It tests your grit.

But it doesn’t mean the end. Remember that insolvency can be reversed.

MSME owners in India should shift their view of insolvency from a personal shortcoming to a fixable financial issue. You’ve got the ability to bounce back.

Ready to Build a More Resilient Business? Access more articles on building a future-proof MSME business.

It’s a financial state, not a legal penalty. It can lead to bankruptcy, a legal revival or shutdown.

The PPIRP, a rescue path for MSMEs, is designed to be completed within a 120-day timeframe.

Yes, if they have given personal guarantees. An orderly exit can help minimise personal liability.

Yes. The debt is an asset. A liquidator will collect it to pay the company’s outstanding creditors.