Suppose…A manufacturing business owner in Hyderabad takes a Rs 25 lakh loan to buy new machinery.

Sales are growing. Orders are coming in.

But three months later, he cannot pay his vendor on time because the EMI, GST dues, and salary payments all hit the same week.

Sound familiar?

This is what happens when business liability is misunderstood or ignored.

Every business, regardless of size or industry, carries liabilities.

The question is not whether you have them. It is whether you are managing them well.

This is where understanding business liability becomes critical.

That’s where this blog will guide you.

Let’s start…

A liability in business is a financial obligation, money your company owes to another party.

This could be a lender, a supplier, the government, or even your own employees.

| For example – Every time your business buys something on credit, takes a loan, or collects GST from a customer before depositing it with the government, a liability is created. Liabilities are recorded on the right side of your balance sheet. They sit opposite your assets. Together, they follow a simple equation – Assets = Liabilities + Equity This means what your business owns (ASSETS) is funded either by what it owes (LIABILITIES) or what the owner has invested (EQUITY). |

Here is what many business owners get wrong.

Liabilities are not automatically BAD.

A loan taken to buy a machine that increases production is a GROWTH MOVE.

But a loan taken to cover last month’s salary gap? That is a WARNING SIGN.

The difference between a healthy business and a struggling one is not the size of liabilities.

It is the intent behind them and the ability to service them.

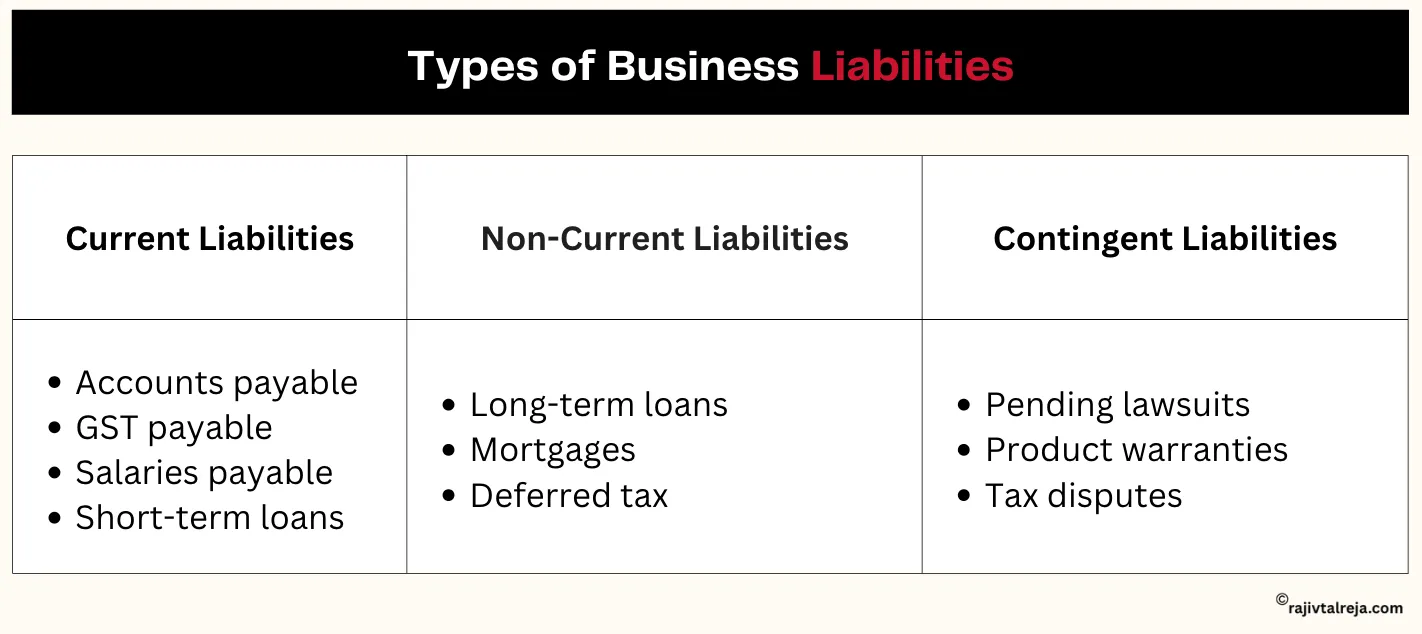

There are three main business liability types.

Each affects your cash flow, planning, and risk differently.

These are obligations due within one year. They directly affect your day-to-day cash flow.

| Accounts payable | Money owed to vendors and suppliers for goods or raw materials already received. |

| GST/Tax payable | Tax collected from customers but not yet deposited with the government. |

| Salaries payable | Wages earned by your team but not yet paid out. |

| Short-term loans | Credit lines, overdrafts, or working capital loans due within 12 months. |

If your current liabilities are consistently higher than your current assets, your business is heading towards a cash flow crisis.

Even if sales look healthy on paper.

These are obligations due beyond one year. They usually fund growth and expansion.

| Long-term loans | Bank loans for machinery, equipment, or business expansion with repayment over 3–5 years or more. |

| Mortgage payable – | If your business owns property financed through a loan. |

| Deferred tax liabilities | Tax obligations that are recognised now but payable later. |

Long-term liabilities are not inherently dangerous.

But if your EMIs cross 40% of your monthly profit, stress begins to build.

You end up working for the bank instead of building wealth.

A contingent liability is a potential obligation that depends on a future event. It may or may not become an actual liability.

Many MSME owners do not even know they carry contingent liabilities.

But ignoring them can hit hard. A single legal dispute can drain lakhs from your business overnight.

Not all liabilities are EQUAL.

Here is how to tell the difference.

| Parameter | Good Liabilities | Dangerous Liabilities |

| Purpose | Funds growth. Machinery, capacity & systems | Covers cash gaps. Salary shortfalls & overdue bills |

| Cash Flow Impact | Generates more revenue than the EMI cost | Drains cash without increasing revenue |

| Repayment Ability | Comfortably covered by monthly profits | Requires borrowing more to repay |

| Example | Rs 15 lakh loan for a new production line | Rs 5 lakh overdraft to pay last month’s salaries |

| Owner’s Stress | Low. Growth feels exciting | High. Sleepless nights & vendor calls |

If your liabilities are helping your business earn more than they cost, you are on the right track.

If they are simply keeping you afloat, it is time to reassess.

| Managing your assets and liabilities correctly is the secret to scaling. Our business coaching programs provide the financial framework you need to take that next step. |

Let us look at real, relatable examples of liabilities in business that cut across industries.

| Liability Type | Example | Who Faces It |

| Accounts Payable | Rs 2 lakh owed to a fabric supplier on 30-day credit | Retail, manufacturing, trading |

| GST Payable | Rs 80,000 GST collected but not yet deposited | Every GST-registered business |

| Salary Payable | Rs 3.5 lakh in team salaries due at month-end | Service, manufacturing, retail |

| Short-Term Loan | Rs 10 lakh working capital loan from the bank | Seasonal businesses, retail |

| Long-Term Loan | Rs 40 lakh machinery loan with 5-year repayment | Manufacturing, construction |

| Contingent Liability | Customer dispute worth Rs 2 lakh, pending resolution | Service, product-based businesses |

| Unearned Revenue | Rs 1.5 lakh advance received for a project not yet started | Service, consulting, events |

Notice how every single business, whether you run a restaurant, a textile unit, or a coaching firm, carries liabilities.

It is universal. What matters is whether you are tracking them and planning for them.

One of the most important things a business owner must understand is distinguishing between liabilities and assets.

They are two sides of the same coin.

ASSETS are what your business OWNS. LIABILITIES are what your business OWES.

Your net worth or equity is the difference between the two.

| Parameter | Assets | Liabilities |

| Definition | What your business owns | What your business owes |

| Balance Sheet | Left side | Right side |

| Effect on Net Worth | Increases it | Decreases it |

| MSME Example | Machinery worth Rs 20 lakh, cash in the bank, and inventory | Bank loan of Rs 15 lakh, vendor dues of Rs 3 lakh, GST payable |

| Goal | Grow, protect, and make productive | Manage, reduce over time, and service on time |

Here is a practical way to think about it.

If you sold everything your business owns today and paid off everything it owes, what would be left?

That is your EQUITY. That is what the business is actually WORTH.

If the answer SCARES you, it is time to take a closer look at YOUR LIABILITIES.

| Understanding your exact financial position is critical. One-on-one business coaching helps you identify the right areas to fix before you take on any new financial obligations. |

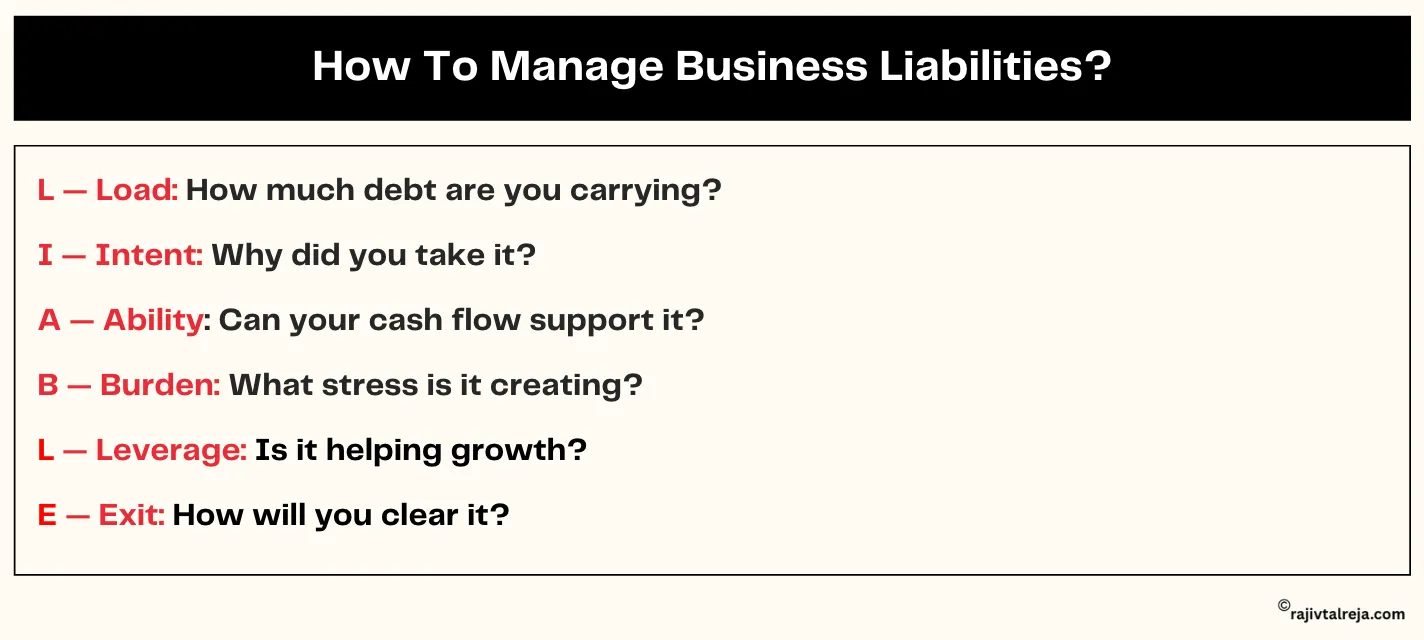

Most articles tell you to “manage liabilities carefully.” But nobody tells you how.

That is why we created the L.I.A.B.L.E Framework.

A simple, practical tool for business liability analysis.

Before you take on any new liability, or when reviewing your existing ones, run it through these six questions.

How much total debt are you carrying right now?

Why did you take this liability?

Can your monthly cash flow comfortably handle the repayment?

If your EMIs plus vendor payments plus salaries exceed 70% of your monthly collections, you are stretched too thin.

What stress is this liability creating?

Is this liability actually helping your business grow?

How and when will you clear this liability?

Use this framework once a quarter.

Sit down, list every liability, and run each one through L.I.A.B.L.E.

You will know exactly which liabilities are working for you and which are working against you.

In our experience working with hundreds of businesses, these are the most common mistakes we see.

Many owners track sales and expenses, but never add up what they owe.

If you do not know the number, you cannot manage it.

Your P&L might show profit.

But if Rs 10 lakh is stuck in receivables and Rs 8 lakh is due in liabilities this week, you are cash-poor despite being profitable.

When one loan is used to repay another, the spiral begins.

This is the most dangerous pattern and one of the hardest to break.

That pending tax notice or customer dispute?

It does not go away because you stopped thinking about it.

Contingent liabilities can become real ones overnight.

Many MSME owners sign personal guarantees without thinking twice.

This means if the business cannot pay, your personal assets, home, savings, and car are at risk.

This feels like a short-term fix.

But it damages trust, affects supply, and often leads to worse credit terms in the future.

The SIDBI Report (2025) notes that the addressable credit gap for Indian MSMEs is approximately Rs 30 lakh crore, which means businesses are either underfunded or borrowing in ways that create more stress.

Business liability insurance protects your company from financial losses caused by third-party claims like injuries, property damage, or professional errors.

For Indian MSMEs, here are the key types of business liability and risk management insurance to consider –

Covers bodily injury to customers or visitors, damage to third-party property, and advertising-related claims.

If a customer slips in your store or a delivery damages someone’s property, this covers the cost.

Also called Errors & Omissions (E&O) insurance.

Relevant if you provide consulting, training, IT services, or professional advice. Covers claims of negligence or mistakes.

If you manufacture or sell products, this covers claims arising from defective or harmful products.

Relevant for businesses that handle customer data online.

Covers costs related to data breaches and cyber attacks.

Many small business owners in India skip liability insurance because they think it is only for large companies.

That is a MISTAKE.

A single customer injury claim or a product defect issue can cost lakhs.

Insurance is not an expense. It is a safety net that lets you focus on growth instead of worrying about what might go wrong.

Business liability is not something to FEAR.

It is something to UNDERSTAND, TRACK, and MANAGE with intention.

Every business carries liabilities from the small vendor bill to the large machinery loan.

What separates businesses that grow from businesses that struggle is not the absence of liabilities.

It is the CLARITY around them.

Learned from this?

Head to our blog for more practical insights on business growth, leadership, and building a business that actually works for you.

Money your business owes, like loans, dues, or unpaid bills.

Current, long-term, and contingent liabilities.

Good if they drive growth; risky if they hurt cash flow.

A future obligation, like lawsuits or warranty claims.

Assets are owned; liabilities are what the business owes.

Loans, salaries, GST, vendor dues, and advances.

Yes, it protects against legal and financial risks.

Keep obligations under 70% of the monthly cash inflow.

It risks insolvency, penalties, and legal action.