Every year on December 12th, people around the globe recognize Universal Health Coverage Day.

If it’s something that is celebrated worldwide, it surely deserves your focus as a business owner.

Allow me to elaborate.

Suppose it’s a Tuesday morning.

Your best sales manager, the one who brings in 30% of your revenue, walks into your cabin.

They look stressed.

They’re not quitting, but they urgently need a salary advance of ₹2 Lakhs because their father just had a stroke.

You want to lend a hand, but your cash flow is tight.

This is a nightmare scenario that many business owners face.

In the post-pandemic world, with medical inflation soaring to 14% in 2024, a single health crisis can drain a family’s savings and distract your employee from their work.

In this blog, we will decode how corporate health insurance benefits can save your business money and safeguard your team.

Many business owners I speak with often see insurance premiums as money going down the drain.

But what if I told you that for every rupee you spend, you could save two in hidden costs?

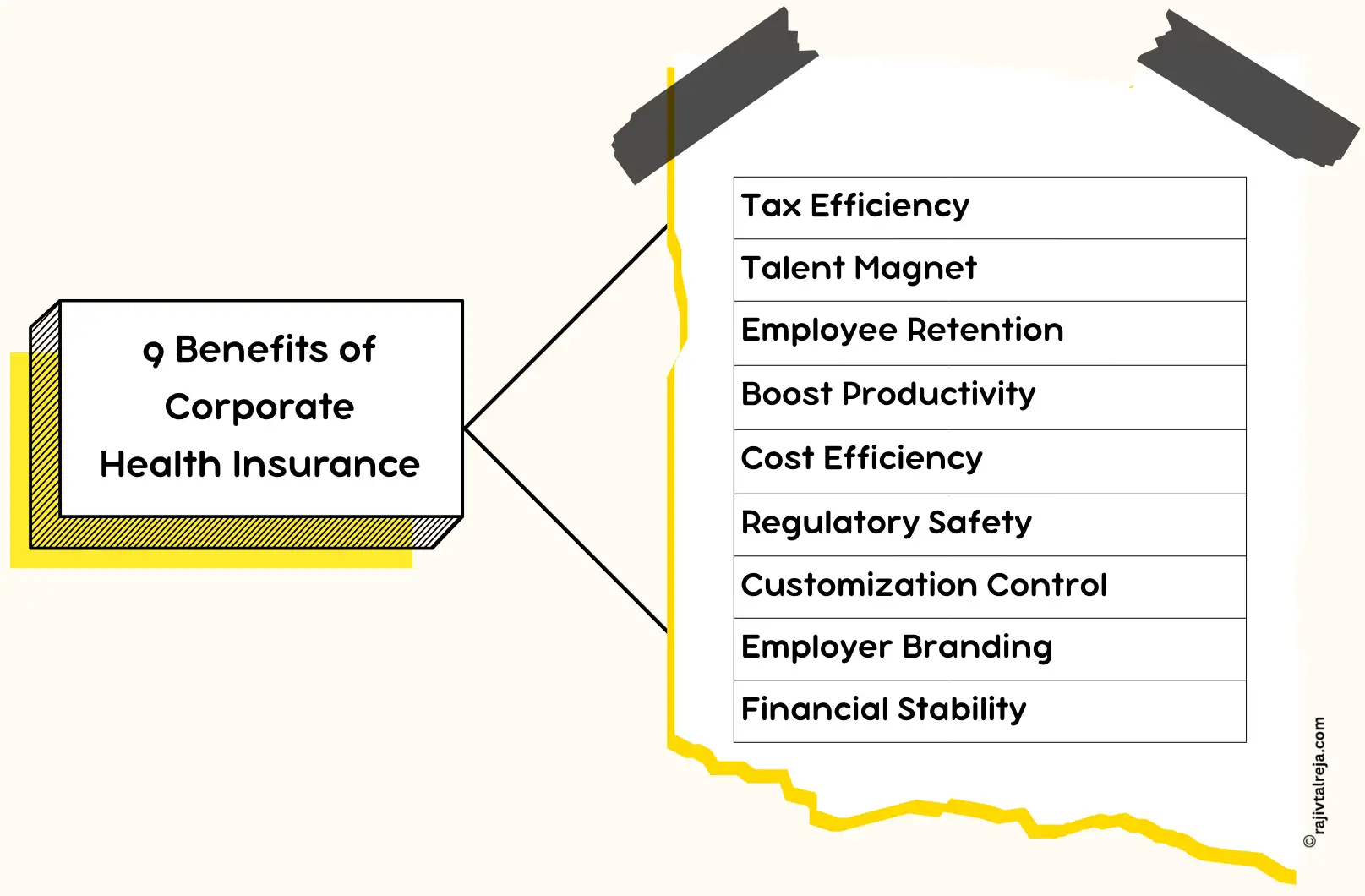

Here’s why small business health insurance can be your secret asset –

This is your biggest immediate win.

The premiums you pay for health insurance for employees in a small business are treated as a legitimate business expense.

You can deduct 100% of this cost from your taxable income under Section 37(1), helping lower your corporate tax bill.

Finding good people is tough.

In a job market where 60% of candidates prioritize health benefits, offering business health insurance helps MSMEs compete with big corporations for skilled talent without having to match their high salaries.

With MSME attrition rates going high, retaining staff is a real challenge.

A small business medical insurance plan creates emotional loyalty.

It makes it harder for employees to leave for a competitor who offers slightly more cash but no security.

Studies show a reduction in absenteeism among insured groups.

Employees return to work faster when they have access to quality healthcare through business medical insurance, reducing “presenteeism” (working while sick but ineffective).

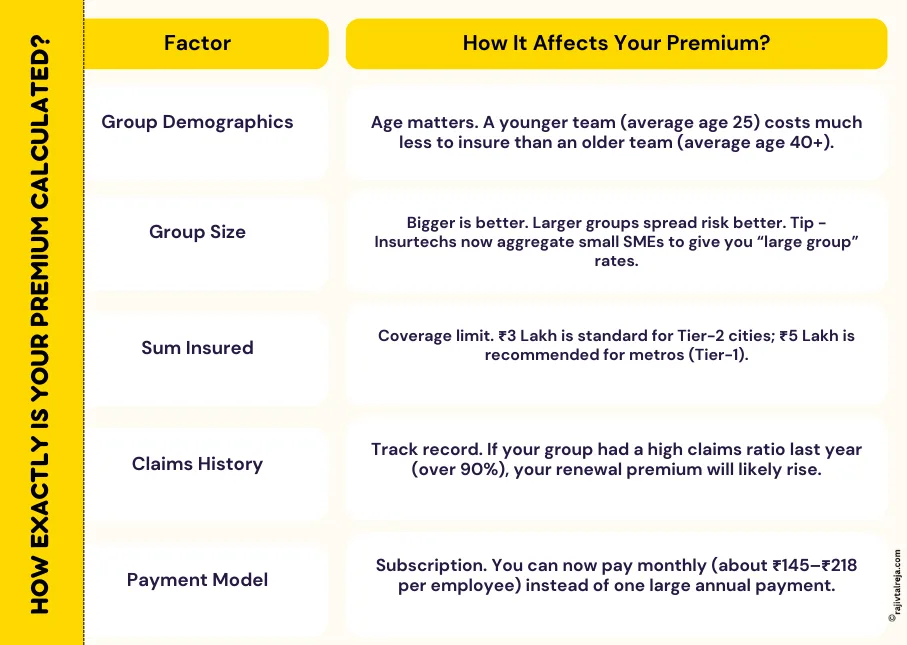

You benefit from “wholesale” rates. By pooling your team’s risk through group insurance for a small business, you can get lower premiums.

This is a fraction of what an individual policy costs.

After the pandemic, having a policy ensures you are compliant with MHA guidelines and Disaster Management Act norms, saving you from potential legal penalties.

Unlike inflexible retail plans, you call the shots. You can waive waiting periods or decide whether parents are covered, tailoring the health insurance plans for small businesses to your exact budget.

It signals that you are a professional organization. This reputation helps attract better vendors and partners who prefer stable, caring businesses.

It prevents you from becoming a bank. When employees face medical crises, they often ask for salary advances.

Small company health insurance transfers this risk to the insurer, protecting your cash flow.

| Do you know? The MSME sector shows a serious “protection gap” in terms of insurance coverage. As of 2025, insurance penetration in the MSME sector is below 15%. Approximately 70% of MSMEs have encountered business risks in the past three years. A large number of MSMEs remain uninsured despite facing these risks. |

Next, we’ll navigate through the legal maze. Do you actually have to buy this?

Let’s find out.

| Once you have your team protected, it’s time to grow. An MSME business coach can help you optimise your revenue and growth to the next level. |

Navigating the rules can be tricky, especially when it comes to knowing what’s mandatory versus what’s just a recommendation.

The regulatory landscape is a mix of strict mandates for low-wage workers and strategic advisories for everyone else.

Here’s a quick overview of the laws that impact health insurance for business owners –

| Regulation | Who It Applies To | Key Mandate for You |

| ESI Act, 1948 | Your employee earns ₹21,000 or less per month (in companies with 10 or more employees). | Mandatory. You must contribute 3.25% of wages. The employee pays 0.75%. Private insurance cannot replace this statutory requirement. |

| MHA Directive (2020) | All industrial and commercial establishments. | Advisory/Standard. After the lockdown, the Ministry of Home Affairs made medical insurance a standard operating procedure (SOP). This is crucial for compliance under the Disaster Management Act. |

| IRDAI Guidelines | Any business purchasing a group policy. | Protection. These guidelines ensure that insurers can’t cancel policies without cause. They also provide Portability, allowing employees to transfer their credits to a retail policy if they leave your company. |

Check the latest updates on the ESI wage ceiling on the official government website.

Now that you’ve got a handle on the laws, let’s explore what these policies actually provide you.

Corporate health insurance benefits have come a long way from the old-school “Mediclaim.”

Thanks to the Insurtech revolution, small businesses now get access to features that used to be exclusive to Fortune 500 companies.

Covers room rent, nursing, surgeon fees, and medicines for illness or accidents.

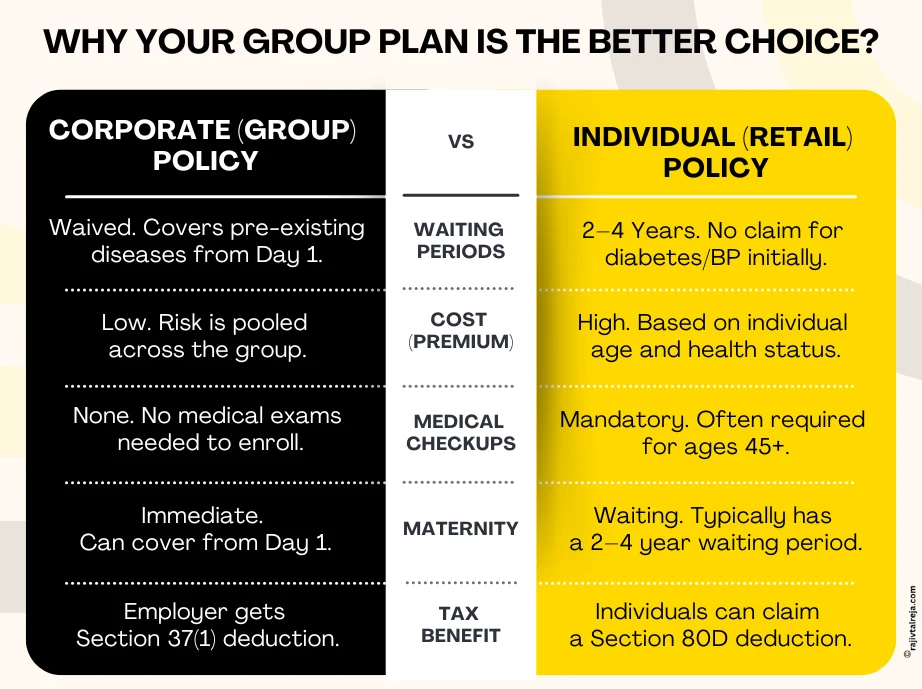

Unlike personal plans that can keep you waiting 2-4 years, corporate plans often waive waiting periods for Pre-Existing Diseases (PEDs) like diabetes.

Your employees are covered right from day one.

You can opt for coverage with zero or minimal waiting periods (9 months), covering delivery and even the baby from birth.

Modern small business health insurance benefits now offer “healthcare” features.

These include tele-consultations, mental health support, and discounts at pharmacies, going beyond just “sick care.”

But hold on, is there only one type of policy? Not at all. You have a whole toolkit to choose from!

Smart owners often mix and match these three types of insurance to balance protection and budget.

When looking for the best health insurance for a small business, consider these structures –

| Plan Type | What It Covers | Best Used For |

| Group Medical Cover (GMC) | Hospitalization. Covers medical expenses (Reimbursement/Cashless) for illnesses and surgeries. | Core Team. Essential for white-collar staff and can extend to their families (Spouse, Kids, Parents). |

| Group Personal Accident (GPA) | Accidents Only. Pays/compensates a lump sum for accidental death or disability (lost limb, etc.). | Field Workforce. Critical for factory workers, logistics teams, or sales personnel. It is very low-cost. |

| Group Term Life (GTL) | Death. Pays a Sum Assured to the family if the employee passes away (any cause). | Retention. A straightforward mortality cover that brings immense peace of mind to families. |

| Do you know? The trend for 2026 is moving toward “Flexi-Benefits” and “Holistic Wellness.” Reports from October 2025 indicate that Mental Health & Emotional Wellbeing have moved from “good-to-have” to “essential” for MSME strategies. |

Before you sign on the dotted line for the cheapest quote, take a moment to dig deeper.

Some low-cost health insurance plans for small businesses have hidden traps that hurt your employees when they need help the most.

Steer clear of “1% Cap.”

Aim for plans that offer “No Capping” or “Single Private Room.”

If capped, the insurer deduces the entire bill proportionately, forcing employees to pay huge amounts.

Day 1 Cover.

Ensure the policy clearly states “0 Day Waiting Period” for Pre-Existing Diseases (PEDs).

Without this, the group health insurance for small business policy won’t be much help for staff with existing health issues like diabetes.

Zero is the ideal.

Try to avoid co-pay clauses of 10–20% if you can.

Co-pay means the employee pays a % of every claim. Use it only for parents to lower premiums.

App-based solutions are a must.

Look for features like WhatsApp claims or HR dashboards

This saves you from hiring an HR person just to manage group health insurance for small business paperwork.

Check Limits.

Ensure there are no low caps on common surgeries like cataracts or kidney stones.

Restrictive limits can leave employees paying out-of-pocket for standard procedures.

| Do you know? A McKinsey India report suggests the sector is at the start of an “S-curve.” Insurtech platforms now allow group policies for teams as small as 7 to 10 employees, breaking the traditional “minimum 50 lives” barrier. |

Now, you know corporate health insurance benefits!

As we gear up for Universal Health Coverage Day on December 12, it’s essential for MSMEs to see corporate health insurance not just as a cost, but as a smart investment.

This investment not only boosts employee well-being and productivity but also helps protect the financial health of the business.

By putting health coverage at the forefront, you’re shifting your mindset from “survival” to “growth“.

So here is what I want to say – “Protect your team, and they will protect your business”.

Ready to build a stronger team? Read our latest blogs on MSME team building strategies here.

Tax savings, talent retention, 25% lower absenteeism, and protection from cash flow shocks.

Hospitalization, maternity, newborns, OPD, wellness, and pre-existing diseases from Day 1.

Yes, corporate plans often waive the 2-4 year waiting period for diseases like diabetes.

Premiums are 100% tax-deductible as a business expense under Section 37(1).

GMC covers illness/surgery, GPA covers accidents/disability, and GTL covers death (any cause).

Yes, many plans cover delivery and newborns with zero or minimal (9-month) waiting periods.

Some plans have room rent caps, co-payments, or sub-limits on surgeries that increase costs.

Look for zero waiting periods, no room rent capping, and app-based claims.