Are you having a hard time getting that important funding approved?

OR

Fed up with long onboarding processes for new clients?

This occurs when your ‘Know Your Business’ process is either delayed or failing.

For many MSME owners, compliance feels like a maze of confusing acronyms and endless paperwork.

However, KYB is important if you want to secure faster funding, establish stronger trust with major partners, and receive better protection against fraud for your business.

This blog will make the KNOW YOUR BUSINESS process easy, transforming it from a compliance headache into your strongest tool for growth and safety.

Know Your Business (KYB) is the process companies use to check if a business they are working with or planning to work with is real and legitimate.

KYB helps you to build better partnerships, stop money crimes like laundering and fraud and protect your hard-earned reputation.

In simple terms, it is a company background check.

A clean KYB profile shows you’re trustworthy and low-risk, which helps MSMEs do business. This is why it matters:

Banks have to do tough KYB checks by law.

Being “KYB-ready” with your papers in order and clear ownership information makes it much more likely that you’ll get loans approved quicker and with better terms.

Big firms are picky about their partners.

Getting through their tough KYB checks shows your small business is serious, open, and dependable. This can lead to valuable deals.

You need to verify the credibility of your partners, too.

Doing your own research keeps you safe from losing money, hurting your reputation, and getting into legal trouble by mistake if you work with a fake or banned company.

You can’t skip getting to know your business partners. If you don’t follow the rules, you’ll face big problems. These can range from big fines to losing the right to conduct business.

Understanding the difference between KYC and KYB matters when you organise your documents and navigate the process without hassle.

The key difference is in what gets verified.

| Know Your Customer (KYC) | Checks verify that an individual is who they claim to be. |

| For example, when you open a personal savings account. |

| Know Your Business (KYB) | Verifies a business entity. |

| For example, it asks, “Does this company exist and is it registered?” and “Who owns and runs it?” |

To verify credibility, you need both.

KYC for companies plays a key role in the KYB process.

| Key Difference | Know Your Customer (KYC) | Know Your Business (KYB) |

| Target | Individual Person | Corporate Entity (Company, Partnership) |

| Main Question | Who is this person? | Does this business exist, and who runs it? |

| Scope | A check on one person. | A thorough look at the company’s structure and all its key people. |

| Documents | Personal ID (Aadhaar, PAN) and proof of where they live. | Company papers (Certificate of Incorporation, GST certificate) PLUS the KYC papers for all owners and directors. |

| Example | Opening a personal savings account. | A bank bringing on a new business client or a small business checking out a new supplier. |

The KYB verification process may look confusing, but it follows a clear order.

If you understand these steps, you’ll be ready for a quick and easy approval when a bank or partner checks you out.

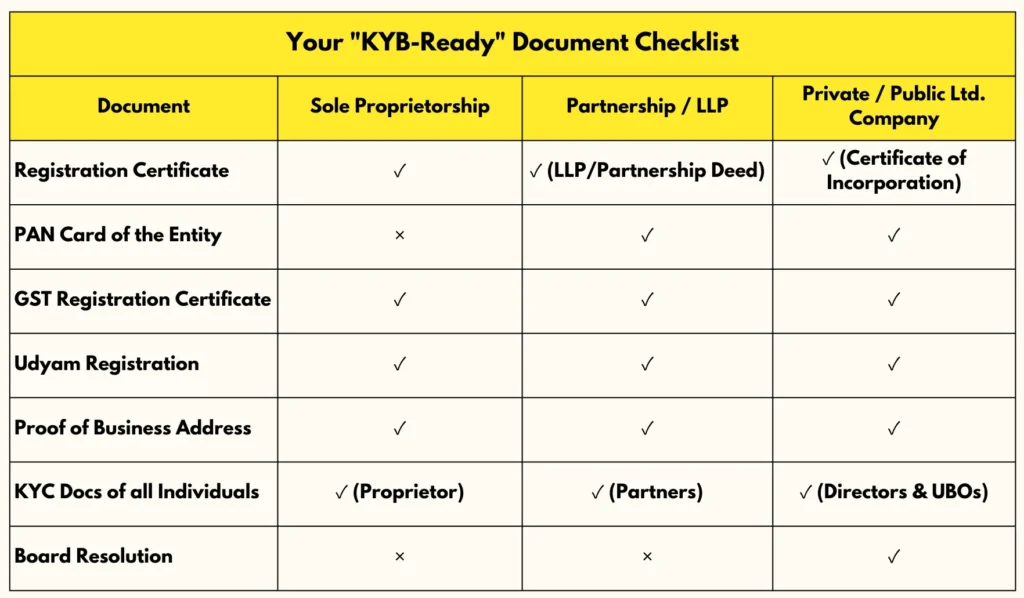

The process begins by gathering your company’s basic identity info – legal name, registered address, CIN/GSTIN, and official business papers like the Certificate of Incorporation, Partnership Deed, and the entity’s PAN card.

The verifier then checks this information against official government sources such as the Ministry of Corporate Affairs (MCA) portal.

They confirm your business’s legal existence, its “Active” status, and whether the director and address details match what you provided.

This step filters out fake companies.

This step has the most importance. It involves looking beyond the corporate structure to find the actual individuals who own or control 10-25% or more of the company.

After identification, each UBO must go through a complete individual KYC check.

Companies then compare the business and its owners to worldwide and local watchlists.

This involves looking for sanctions (like those from the UN or OFAC), links to Exposed Persons (PEPs) who might increase corruption risk, and any negative news stories connecting the business to fraud or legal troubles.

Today’s compliance needs ongoing checks.

Businesses are perpetually screened for any changes to spot any changes, such as a new director ending up on a sanctions list.

This keeps things in line throughout the whole business relationship.

The KNOW YOUR BUSINESS requirements you face have their roots in a strict legal framework that aims to protect the whole financial system.

Understanding why these rules exist can help you deal with them more effectively.

The Reserve Bank of India (RBI) turns the PMLA’s requirements into specific operational rules for banks through its Master Directions on KYC.

These rules say that banks must –

Breaking the rules comes with harsh punishments.

Let’s understand how you do this practically.

Here’s your two-part guide to nailing the know your business process. It’ll help you clean up your own act and shield yourself from dodgy partners.

To get fast approvals for loans and contracts, your MSME needs to be “KYB-ready.” This means having a comprehensive digital document kit prepared.

Scan these documents and store them in a digital folder.

Also, make sure you have a professional website and a business email address to create a verifiable online presence.

You can’t afford to do a full bank-level check on every partner, but you can use a smart, risk-based method.

The way to get to know your business partners depends on how valuable the relationship is.

Look up the business name and who owns it to find their website, what people say about them, and any news stories.

Pull up Google Maps to see if their address looks like a real business place.

Give their phone number a call and send a quick email to test.

If it’s a company or LLP, check on the Ministry of Corporate Affairs site to see if they’re registered and who’s running the show, all for free.

Check their GSTIN to make sure their legal name and how they’re set up as a business check out.

Get them to send over their business PAN and proof they’re registered, then compare these with what you’ve found out.

If the client is big, then request them for a formal list of their Ultimate Beneficial Owners.

To get the best protection, think about using automated KYB platforms from KYC companies that specialise in this.

These tools can check partners against global watchlists and news sources, providing screening at a price that small businesses can afford.

Business verification is changing, and it’s important for you to comply with it.

Don’t see KYB as a chore, but as a key skill. Being proactive builds trust, helps you get funding, and keeps your name clean. Utilise technology and good business practices to turn following the rules into your edge for long-term growth.

You’ve learned how to handle KYB. Now, click here to explore more article to streamline your operations and grow your MSME.