Two group companies work together to develop a product.

Both invest money, people, and intellectual property.

Now the product is profitable. The question is… who gets how much?

This is exactly the problem the profit split method solves.

It is one of the five transfer pricing methods recognised by the OECD and under India’s Income Tax Act (Section 92C).

Most articles on this topic stop at definitions.

This blog changes that.

We’ll walk you through the profit split method of transfer pricing with real numbers, a decision framework, industry examples, and the mistakes that land companies in disputes.

The profit split method (PSM) is a transfer pricing method that looks at the combined profits earned by two or more related entities from a controlled transaction.

It then splits those profits based on the relative value of each entity’s contribution.

For example…

| Two group companies collaborate on a project. One handles the R&D. The other manages marketing and distribution. Both contribute something valuable. The profit split method figures out how to divide the combined profits between them in a way that reflects what independent companies would have agreed to. |

This concept is called the arm’s length principle.

Under Indian tax law, Section 92C of the Income Tax Act lists the profit split method as one of the prescribed methods for computing the arm’s length price of international transactions.

And choosing the right method matters more than most business owners realise.

| India’s transfer pricing jurisprudence has generated over 10,000 reported rulings, one of the highest volumes in the world, reflecting how actively tax authorities scrutinise related-party transactions. |

Pick the wrong method, or apply it poorly, and it directly affects how much tax your business pays.

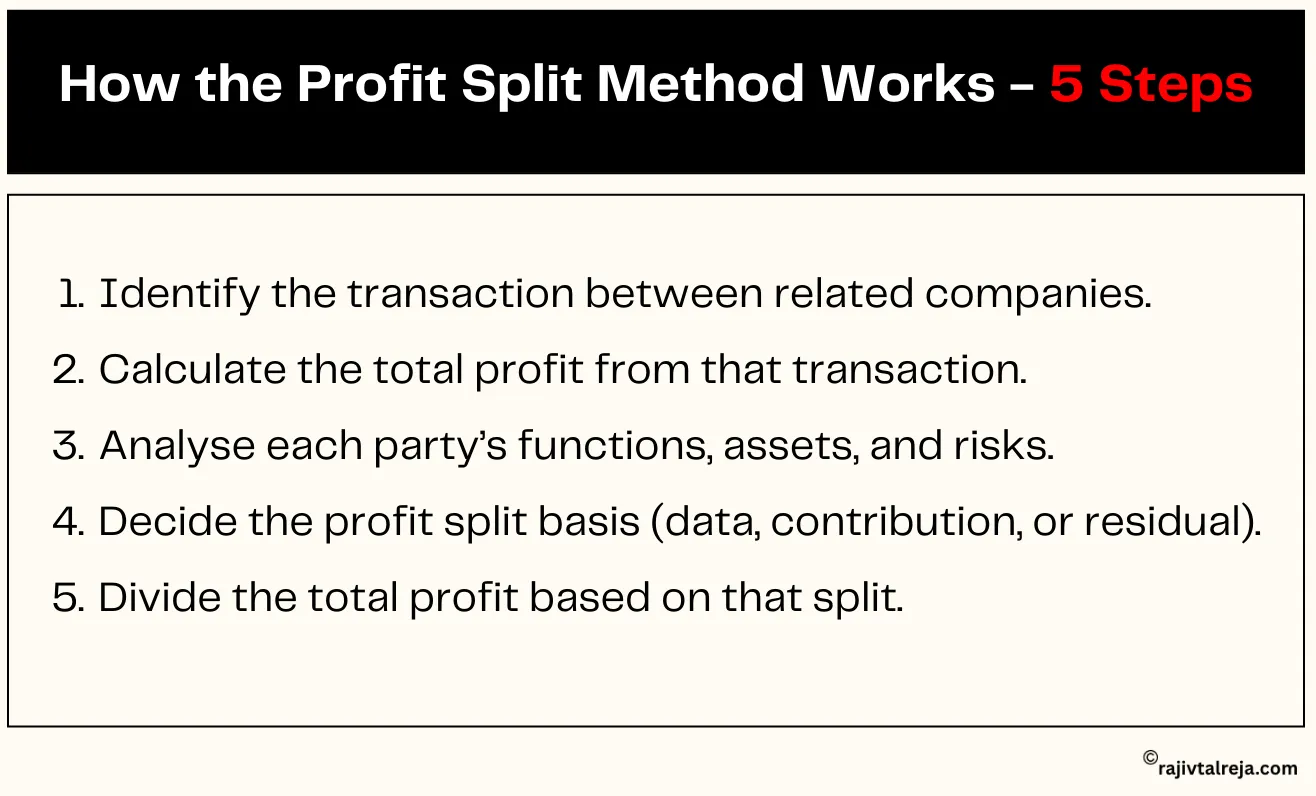

Let’s break this down into a simple, step-by-step process.

Understanding how the profit split method works becomes much easier when you see it with actual numbers.

Pinpoint the specific transaction between related entities that needs to be tested.

This could be joint product development, shared manufacturing, or co-branded marketing.

Calculate the total profit earned from this transaction across both entities.

Use a common accounting standard and a uniform currency before combining.

Map out what each entity actually contributes – functions performed, assets used, and risks assumed.

This is the backbone of the entire method.

Decide how to divide the profit – based on comparable data from independent transactions, the relative value of each party’s contribution, or a two-step residual approach.

Apply the chosen split factor and assign each entity its share.

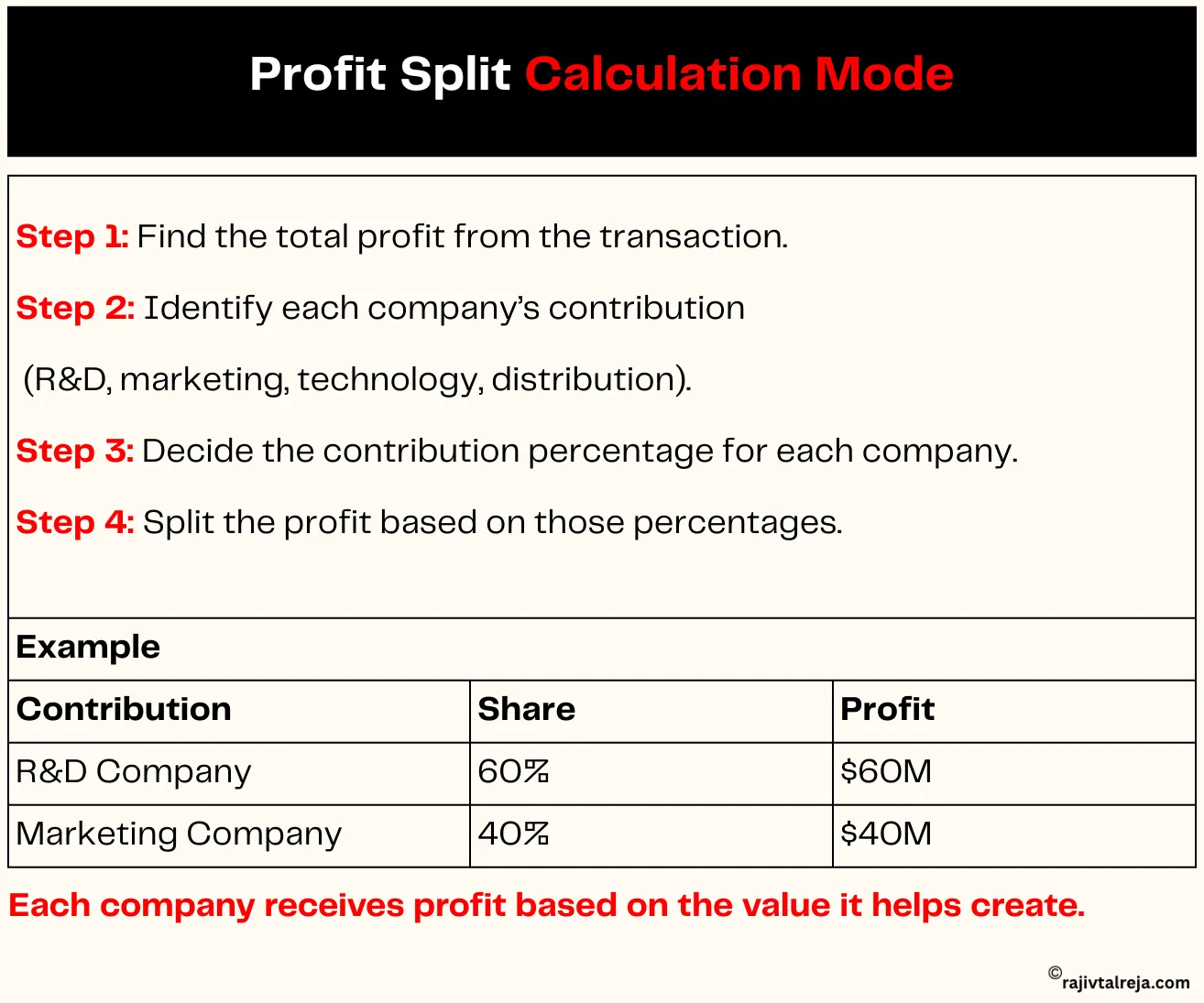

The FORMULA is straightforward:

Entity’s Share = Combined Profit × (Entity’s Contribution / Total Contribution)

So, Entity B’s share = ₹50 Crore × 60% = ₹30 Crore. Entity A’s share = ₹50 Crore × 40% = ₹20 Crore.

This is a simplified contribution-based profit split.

In practice, the functional analysis behind these percentages is detailed, documented, and backed by evidence.

| These five steps ensure compliance, but scaling requires a strategy. Discover how business coaching helps you build a bulletproof corporate structure. |

There are three recognised approaches to applying the profit split method.

Each works differently depending on the data available and the nature of the transaction.

The comparable profit split method uses external data from similar transactions between independent (unrelated) companies.

If you can find a comparable deal where two independent parties split their profits, that ratio becomes your benchmark.

This method is ideal when reliable comparable transaction data is actually available.

In practice, though, finding truly comparable profit splits is rare, which limits how often this approach is used.

This approach divides the combined profit based on the relative value of each party’s contribution functions performed, assets deployed, and risks assumed.

It’s the most commonly used version of PSM.

When both entities make significant, measurable contributions to the transaction, this method captures the full picture.

This is a two-step process.

First, each entity receives a routine return, a basic arm’s length compensation for standard functions.

This is usually calculated using another method like TNMM or Cost Plus.

Second, the remaining “residual” profit is split based on each party’s unique and valuable contributions, typically intangible assets like IP, proprietary technology, or brand value.

This method is best suited when both parties bring something unique to the table, R&D, patents, or specialised know-how that cannot be benchmarked against independent transactions.

| Type | How It Works | Best Used When | Complexity |

| Comparable PSM | Uses external data from similar uncontrolled transactions | Reliable comparable transaction data exists | Low–Medium |

| Contribution PSM | Splits based on the relative value of each party’s contributions | Both parties make significant, measurable contributions | Medium |

| Residual PSM | Routine returns first, then the residual is split by unique contributions | Unique intangibles, R&D, or IP are involved | High |

Here’s a simple decision framework.

TNMM (Transactional Net Margin Method) is a one-sided method.

It tests the net profit margin of one entity against comparable independent companies.

It works well when one party performs routine functions, and the other is the “tested party.”

The profit split method, on the other hand, is two-sided.

It evaluates both entities.

It’s the better choice when both parties contribute something unique and valuable that cannot be easily benchmarked.

Here’s when to pick which:

| Scenario | Best Method | Why |

| Both parties contribute unique IP | Profit Split | Captures contributions from both sides |

| Routine distributor with limited risk | TNMM | One-sided analysis is sufficient |

| Highly integrated supply chain | Profit Split | Transactions cannot be evaluated separately |

| Benchmarkable entity with standard functions | TNMM | Comparable net margin data is available |

| Joint R&D or shared intangible development | Profit Split | No single party owns the full value |

| Contract manufacturer with a cost-plus model | TNMM | Simple, routine function – cost-plus benchmarks work |

Most blogs on this topic use vague “Company A and Company B” examples.

Let’s look at how the profit split method actually applies across real industries.

A parent company owns a drug patent.

A group entity in India handles formulation, regulatory compliance, and distribution.

Both entities contribute valuable IP.

One owns the molecule, the other navigated a complex regulatory landscape.

The combined drug profits are split based on each entity’s R&D investment and risk exposure.

A global tech company builds the platform.

A regional entity in India manages user acquisition, localisation, and marketing. Both create value: the platform IP and the local customer base.

PSM splits the platform revenue based on the relative value of technology versus market development contributions.

Two group companies collaborate to build a SaaS product.

One writes the core code.

The other builds integrations, handles testing, and manages client onboarding.

Since both contribute to the IP, a residual profit split works well, routine functions get a base return, and the residual profit is divided based on unique contributions to the software.

A multinational brand owner licenses its brand to an Indian subsidiary.

The subsidiary invests heavily in local advertising, building the brand’s presence in India.

Both parties contribute to the brand’s profitability in the Indian market.

The profit is split based on the brand owner’s IP value versus the subsidiary’s marketing investment.

Every transfer pricing method comes with trade-offs.

Here’s a clear look at both the advantages of the profit split method and disadvantages of the profit split method, side by side, so you can weigh them before choosing this approach.

| Advantage | Disadvantage |

| Two-sided, holistic analysis | Complex and expensive to implement |

| Works when comparables don’t exist | Requires extensive data from all entities |

| Handles complex intangibles well | Subjective split factors |

| Reduces double taxation risk | Measuring intangible contributions is difficult. |

| Aligned with arm’s length principle (OECD) | Heavy documentation burden |

| Shares risk fairly between entities | Internal disagreements are common |

The profit split method is powerful when used correctly.

But it demands rigour.

If your functional analysis is thin, your data is inconsistent, or your documentation is weak, the disadvantages will outweigh the advantages every time.

Most articles only talk about when to use PSM.

Nobody discusses when it fails.

Here are the scenarios where applying the profit split method becomes risky or outright incorrect.

| Scenario | Why PSM Fails Here? |

| One party performs only routine functions. | If one entity is a simple contract manufacturer or routine distributor with limited risk, PSM is overkill – the two-sided analysis adds complexity without value |

| Reliable comparable data exists | PSM is designed for situations where comparables are unavailable. Using it when simpler methods apply invites scrutiny from tax authorities |

| Financial data across entities is inconsistent | If entities use different accounting standards, fiscal years, or cost classifications, the combined profit figure becomes unreliable. Garbage in, garbage out |

| Arbitrary contribution percentages are used | A 50:50 split “because both parties are important” is not a defensible position. Tax authorities will reject allocations not backed by functional analysis |

| The cost of implementation exceeds the benefit | For smaller transactions or those with limited profit at stake, the complexity and expense of a full PSM analysis may not be justified.d |

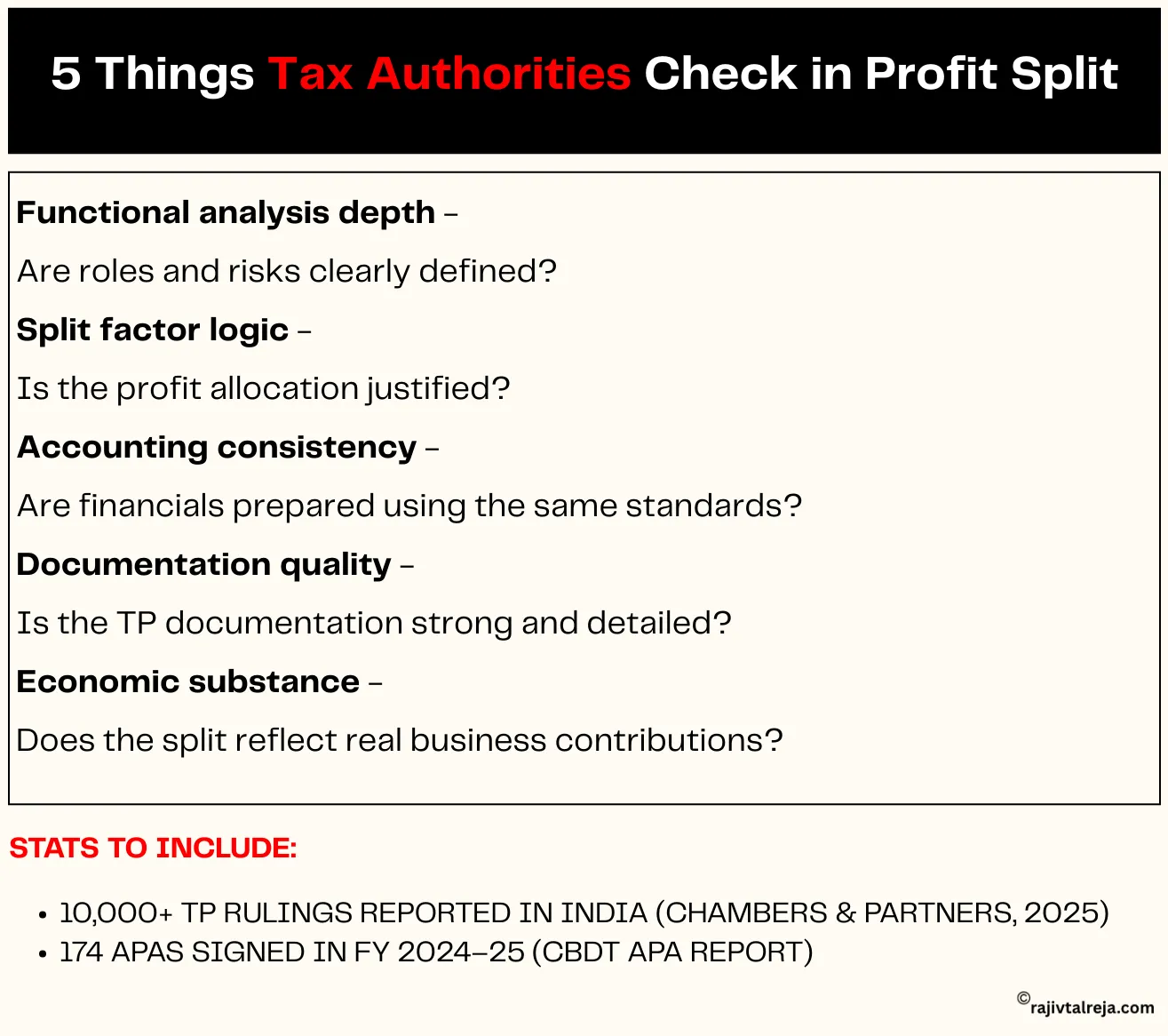

| India’s transfer pricing landscape is one of the most active in the world. According to Chambers & Partners (2025), there are over 10,000 reported transfer pricing rulings in India. In FY 2024-25, the CBDT signed a record 174 Advance Pricing Agreements (APAs), taking the cumulative total to 815. In India, if the Transfer Pricing Officer (TPO) disagrees with your profit split, the dispute typically goes to the Dispute Resolution Panel (DRP) or the Income Tax Appellate Tribunal (ITAT). |

The process can take years. Getting it right the first time saves a lot of pain.

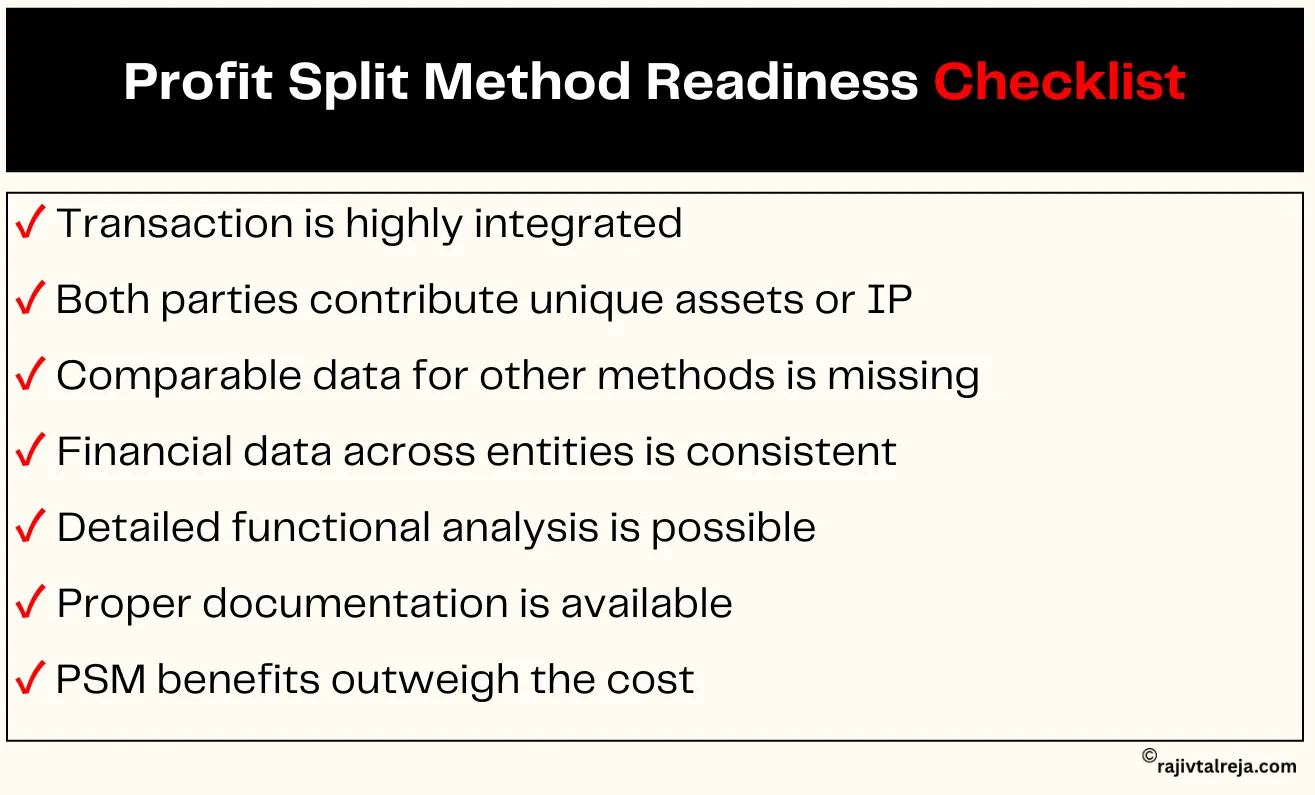

Before you apply the profit split method, run through this checklist.

If you can’t check most of these boxes, PSM may not be the right method for your transaction.

If the related entities work closely together on a shared activity where value creation is interlinked, PSM is appropriate.

If one or both parties bring IP, proprietary technology, specialised know-how, or brand value to the transaction, PSM can capture that value.

If you cannot find reliable external benchmarks for CUP, Cost Plus, or TNMM, PSM is likely the most suitable alternative.

Before combining profits, ensure both entities use consistent accounting standards, cost classifications, and reporting periods.

You need detailed information about each entity’s functions, assets, and risks. If this data is not accessible, PSM will be difficult to defend.

PSM requires comprehensive transfer pricing documentation. Ensure your team or advisors can maintain this over time.

The expense of building and maintaining a profit split model should be proportional to the transaction value and tax risk at stake.

What Data Is Required?

Detailed financial statements from all entities, a thorough functional analysis, contribution breakdowns with supporting evidence, industry benchmarks where available, and consistent accounting policies across all parties.

These are not theoretical disadvantages.

These are the actual mistakes we’ve seen that cause disputes, audits, and costly adjustments.

| Common Mistake | What Goes Wrong | How to Fix It |

| Arbitrary split ratios (e.g. 50:50 by default) | Tax authority rejects the allocation as unsupported | Base ratios on functional analysis and contribution data |

| Weak or incomplete documentation | Audit flags, penalties, and prolonged disputes | Maintain a detailed TP study with supporting evidence |

| Ignoring functional analysis | Contributions assumed, not proven – authorities reject the model | Map functions, assets, and risks for each entity separately |

| Inconsistent accounting standards | Combined profits are unreliable and open to challenge | Align accounting policies before combining financials |

| Static model – never updated | Business evolves, but the profit split stays the same | Review and update the PSM model annually |

| Don’t let financial missteps create daily chaos. Working with the best business coach ensures your business is built on solid, audit-proof frameworks. |

The profit split method is not the easiest transfer pricing method to implement.

But for the right transactions, highly integrated, involving unique contributions from both sides, it’s often the most accurate and defensible.

The key is in the execution.

If your business involves related-party transactions where both entities bring real value to the table, understanding the profit split method is not optional. It’s a core part of getting your financial management right.

Learned from this?

Head to our blog page for more practical insights on business growth, leadership, and building a business that actually works for you.

It splits combined profits between related entities based on each party’s contribution value.

It uses profit ratios from similar independent-party deals as a benchmark for allocation.

Identify the transaction, calculate the combined profit, analyse contributions, and then allocate.

The profit split method analyses both entities equally. TNMM tests only one party’s net margin against comparables.

It handles unique intangibles, integrated operations, and reduces double taxation risk.

It is complex, data-intensive, and the choice of split factors can be subjective.

When both parties contribute unique intangibles and transactions are highly integrated.

Yes, it applies to specified domestic transactions exceeding ₹20 Crore under Section 92BA.

Arbitrary split ratios, weak documentation, and treating the allocation as a one-time exercise.