Your books show profit, but your bank account is empty.

You’ve made the money, sent out invoices, and your Net Income looks good on paper.

Yet, you still worry about paying your staff or the next supplier bill.

This gap between PROFIT and actual CASH can be risky.

This fix is: Cash flow from operating activities.

This blog will help you understand this gap and how to fix this problem in a few simple steps

Let’s start with basics…

It’s the cash your main business activities generate.

The money coming in from selling products or services and going out to cover core costs like rent, materials, and salaries.

This is your primary operating cash inflow.

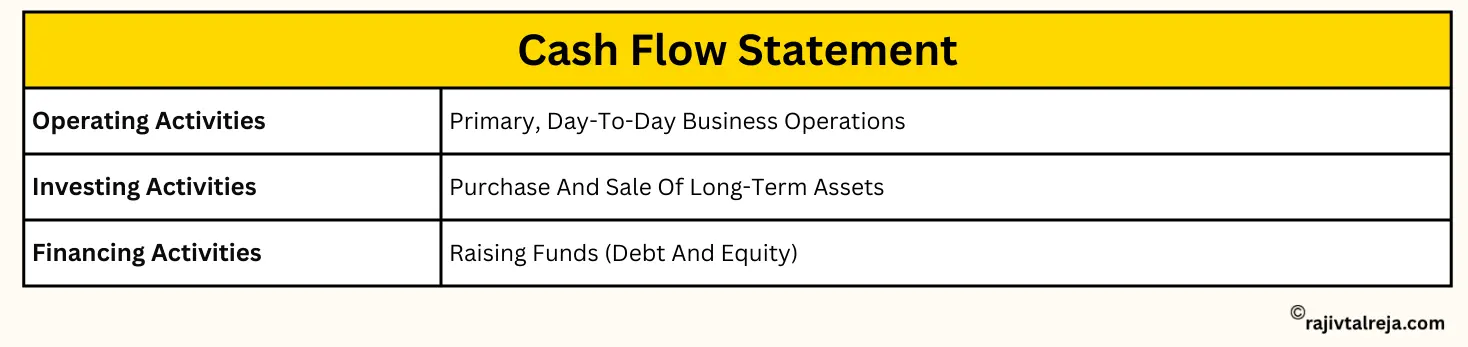

All cash movements fall into three main categories:

INVESTING, OPERATING and FINANCING activities.

The core of your business (making and selling your product).

These are the day-to-day functions that generate revenue.

Some common operating activities examples include collecting cash from customers and paying suppliers.

Buying or selling assets like equipment or property.

The cash from these transactions is reported on the statement of cash flows investing activities section.

Working with owners or lenders (loans, debt repayment, owner payouts).

A strong cash flow from operating activities is the best way to check your business’s short-term health.

It shows whether your core activities can keep running without needing extra loans or selling assets.

| Financial clarity is the foundation of growth. A business coach can help you turn this clarity into a scalable action plan. |

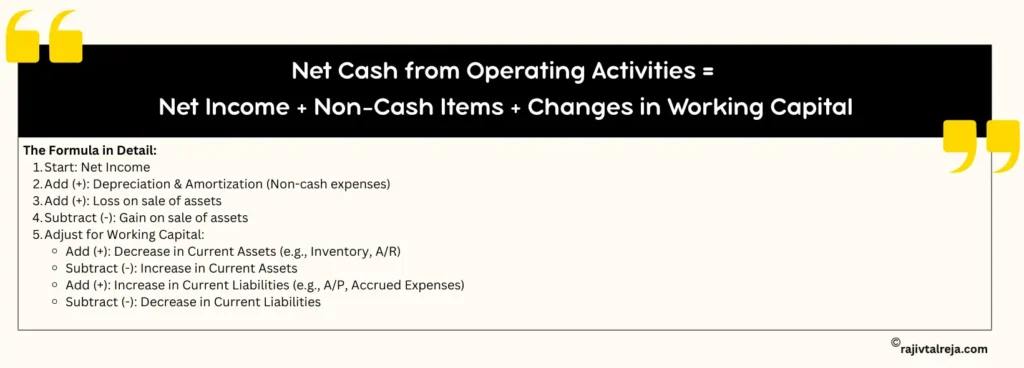

For a busy MSME owner, the easiest and most revealing way to calculate cash flow from operating activities is the INDIRECT METHOD.

This starts with the Net Income from your Income Statement and adjusts for the difference between accounting profit and actual cash flow.

It’s a helpful tool that shows why your profit doesn’t match your cash.

Here’s the formula to find your net cash inflow from operating activities:

Start with the bottom line of your INCOME STATEMENT.

This shows the profit you earned using the accrual method, which records revenue when it’s earned and expenses when they occur, not when cash moves.

The first adjustments focus on expenses that lowered your Net Income but didn’t involve actual cash spending.

Since these didn’t reduce cash, you need to add them back to Net Income.

| Non-Cash Item | Effect on Cash Flow | What It Means |

| Depreciation and Amortization | Add Back | These are write-offs for old assets. You paid the cash years ago, so no money leaves the business now. |

| Loss on Sale of Assets | Add Back | Selling an asset counts as an investing activity. The loss reduced profit, but you remove it to see the true operating cash flow. |

| Gain on Sale of Assets | Subtract | The gain increased profit, but the cash received is part of investing. Subtract it to keep operations separate. |

| If your profits are disappearing into these “adjustments,” a business coach can help you decode these financials to understand what’s really holding you back. |

This step looks at the gaps between when you record revenue or expenses and when the cash actually moves.

Working capital is what’s left after subtracting the difference between current assets and current liabilities.

| Change in Working Capital | Effect on Cash Flow | Why It Happens |

| Accounts Receivable Goes Up | Subtract | You made sales on credit but haven’t received the cash yet. Customers delaying payment ties up your cash. |

| Accounts Receivable Goes Down | Add Back | You collected cash from earlier sales. This money wasn’t counted in this period’s profit, so now it’s available. |

| Inventory Goes Up | Subtract | You bought more stock than you sold. Cash is now tied up in inventory. |

| Inventory Goes Down | Add Back | You sold more stock than you purchased, turning inventory back into cash. Cash is freed up. |

| Accounts Payable Goes Up | Add Back | You received goods or services but haven’t paid suppliers yet. This keeps cash in your pocket, like an interest-free short-term loan. |

| Accounts Payable Goes Down | Subtract | You paid suppliers more than the cost of new purchases, using cash to clear old debts. |

Go through these three steps:

Start with Net Income, add back Non-Cash Expenses, and adjust for Changes in Working Capital.

At the end, you get the key figure: your cash flow from operating activities.

A strong positive number for your net cash inflow from operating activities shows your business is healthy and can keep going.

Mastering cash flow from operating activities is a key to running your business’s money well.

Don’t let money worries control your decisions.

Start using cash as your primary measure today.

Regularly monitoring your cash flow from operating activities will provide clarity.

If you want to move your business from “making money but always broke” to truly stable and thriving…

Check your monthly CFO report, see where cash is stuck (like in A/R or inventory), and start applying one of the hands-on fixes shared earlier this week.

Looking for more financial strategies to scale your business? Check out our blogs on growth strategies for MSMEs.

Common examples include collecting cash from customers and paying suppliers, rent, or salaries.

Use the Indirect Method: Start with Net Income, add non-cash items, and adjust working capital.

The formula is: Net Income ± Adjustments for Non-Cash Items ± Changes in Working Capital.

It is the cash generated by your main business activities, like selling products or services.

All cash movements fall into investing, operating and financing activities.

It reports cash from buying or selling assets, distinct from your core operating cash inflow.

Start with Net Income from the P&L, then adjust for non-cash expenses and working capital changes.